Financial accounting is the language of business

No question. It’s how investors, managers, creditors, suppliers, and regulators keep track of the “score”. Without it, even the most basic questions like “how much profit did you make” would require hours of meetings, persuasion and probably significant disagreement. It would be like talking without using verbs. It would work – eventually – but painfully.

You have to know the basics

Consultants without a strong understanding of the the vocabulary, frameworks and principles, are certain to embarrass themselves in front of the client. If you don’t immediately know what A = L + E stands for in accounting, then you need to do some remedial studying. As an exercise, read the Economist Business section, and stop whenever you don’t understand something related to a financial statement and look it up.

It seems perfect, but it’s not

On the surface, accounting seems like a monolith of precision, rules, and conservatism; something hallowed, balanced and almost scientific. After all, the financial statements tick-tie with each other, articulating perfectly. Financial statements are permanent and accessible – all online, ready for reading. The GAAP and IFRS guidelines tell what we can, cannot do. Don’t want to go to jail.

This makes accounting seem more immutable than it is. Savvy consultants know that financial statements are the basics, but far from the whole story. Here are several reasons financial account is imperfect. For the CPAs, feel free to “pile on”.

The Good (the quirky way accounting works)

1. Accrual accounting

Cash accounting is very brutish – it counts how much cash you spent or have at the end of the quarter and it ends there. Simple, but misleading.

In contrast, accrual accounting attempts to fix this by dividing up the revenue or expense and matching it to the right time period. The easiest example is the depreciation on equipment; if you run a printing shop and pay $700K for a piece of machinery, your accountant will stop you from writing that up as a one-time expense. No, no, no. Since the equipment will likely be used for 7 years (as an example), you can only deduct 1/7th of the value (-$100K) per year as an expense. Better, not perfect.

There are a dozen types of accrual accounts which essentially fall into these pre-paid and accrued expenses and income. You can see this type of splitting, pulling-in, pushing-out of expenses throughout the balance sheet.

2. Historical costs

Accounting by its nature is going to be conservative, so it forces companies to value things at their acquisition cost. This will understate assets that have appreciated (like a corporate headquarter building in Manhattan that was purchased 30 years ago), or overstate assets that have lost value (e.g., was MySpace really worth $580MM when Rupert Murdoch bought it?). This is why some investors are lobbying McDonalds to spin off the real estate of their locations into a REIT to unleash the historical cost value trapped in the shares here.

The Bad (oddities and things to be aware of)

3. One-time events

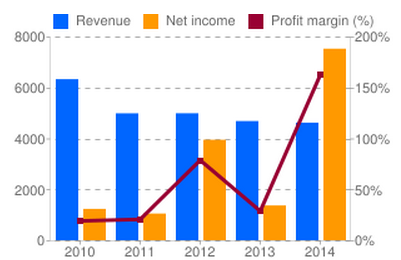

As with any analysis, you want to look at things when it is in “steady-state”; to see the trend, extrapolate a forecast, or guesstimate the future, you want to look at a base case. Clearly, making assumptions on spikes and blips in profitability would be stupid. As such, keep an eye out for large non-reoccurring expenses or gains – anything that does not occur during the ordinary course of business. A few examples, Yahoo records a huge bump in earnings because of a $9 billion windfall from the IPO of Alibaba. That is not normal. Look at the graph below, the orange bar goes from: low, low, low, low, CRAZY high. Not normal.

4. Management Discussion and Analysis (MD&A)

This is where the management brings up all the most salient points (revenues, costs, financing, competition etc). Of the hundreds of pages of a 10K, these are the 10 pages you always read. Inside this narrative, you can often find lots of hidden details which the company needs to disclose (changes in depreciation schedule, changes in accounting treatment etc) which they don’t really want to brag about. All the tidbits can add up to a dramatically different look at the financials.

The Ugly (tips, tricks, secrets)

The public markets are ruthlessly competitive and analysts are continually peer-pressuring companies to beat increasing expectations. Executives work collectively to meet their quarterly numbers, sometimes through overly aggressive interpretation of the financial accounting rules. (Ominous music starts playing in background). Some of the ways that that companies and managers bend accounting rules in their short-term favor, which are (more or less) legal might include:

- Loose revenue recognition (sales that are not exactly finished)

- Inadequate accrual for expenses (no saving enough to pay for the expense)

- “Cookie jar” reserves: company accrues extra expenses when times are good (putting a cookie in the jar for a rainy day), so that when earnings are down, they can reduce their reserves (take a cookie out)

- “Big bath” one time charges. Companies are fairly notorious for dumping all their losses and questionable accounting practices into 1 big non-recurring loss. It’s like they take out ALL of their garbage at one time. Analysts are trained to overlook these 1 time events, and this can hide structural problems elsewhere.

- “Stuffing the channel” Companies sometimes push extra product to their distributors (stuffing product in the sales channel) so it inflates sales short-term. The SEC has litigated several companies for doing this. Al Dunlop from SunBeam was one of the most famous offenders here.

The list of accounting “improprieties” can go on and on, but you get the idea. Companies steal revenue from future periods, or create “cookie jars” of savings to use at a different time, all in the effort of smoothing out earnings. Financial accounting is a series of rules, and any good mobster will tell you, “rules were meant to be broken.”

As a consultant, be aware of the good, bad, and the ugly. We don’t break rules, we don’t help clients break rules. That said, we need to know how people would do it – so we can be on the watch out.

After following your advice for the free online education I am know able to understand A = L + E immediately. 😉 To make it more serious I did not go for the free version but enrolled for the signature track to make sure that I actually stick to it and finish it. Thx for the great recommendation in “Accounting literate?”! My recommendation to everyone who wants to fresh up or get started in accounting!

Good for you. Which class did you enroll for, the Coursera one with the Wharton professor?

Thank you for writing this informative blog. I’d like to understand the process further of the spin off of the existing McDonalds locations into a REIT. So, the stated value on the Balance Sheet would be of a lower value than today’s value ….. where/how does the REIT come into play?

Heh heh. It’s been a while since I wrote that post – so will have to do the review and study of the topic.

That said, I would argue yes, McDonalds believes they can get more value (shares x listing price) if a separate entity vs. built inside of MCD valuation. Fundamental logic or divestitures or carve out.

Aaahhh gotcha! Ah ha moment! That you for sharing your knowledge.

Nicole