In sharp contrast from the last post about slow global growth, BCG writes in their 10th annual report about emerging market companies that are killing it. BCG notes that the top companies – i.e. highlighted in this report – are growing revenues at 3x the market with above average margins. The old days when multi-national firms from the US, Europe, Japan were easily capturing market share in international markets are O.V.E.R. It’s actually the other way around – with global challengers (top 100), and global champions (next 1,500) killing it. Read the BCG report here (35pg) or read this post.

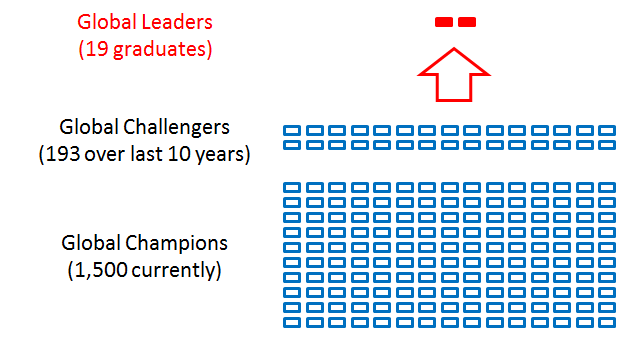

Three categories: 1) Global leaders like Gazprom, Tata Consulting, Tata Motors etc who are in the Global Fortune 500 from the emerging markets. 2) Global Challengers who are giving market leaders a run for their money 3) Global Champions who do great work, but still largely on a regional scale.

BCG tracks 1,500 champions, and over the last 10 years there have been 193 global challengers. Of the challengers, 19 of them have “graduated” to the big leagues. Took me a couple of readings to get it, but this is my visualization of the hierarchy. If I have any BCG readers – please correct me, if wrong.

Fast growing and profitable

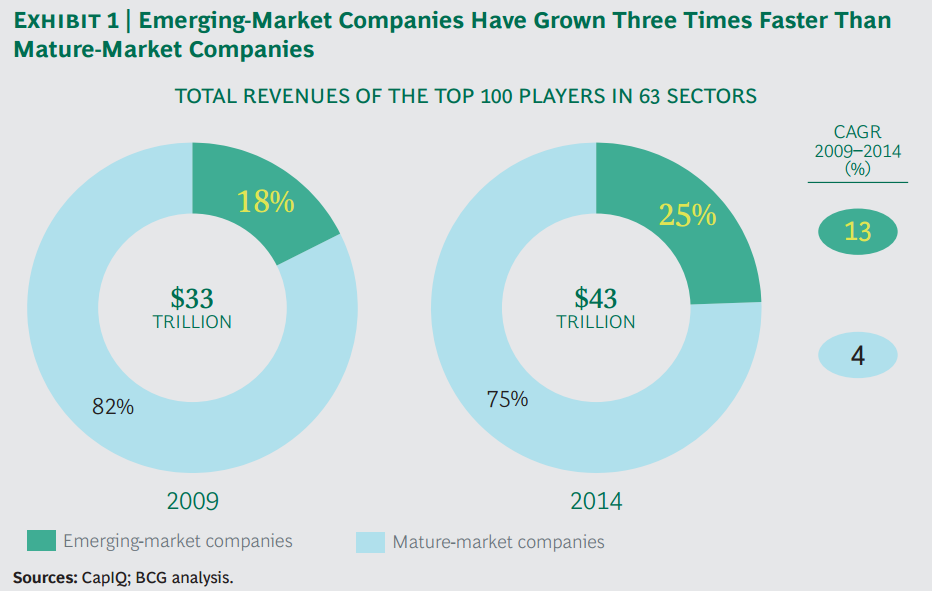

Yes, most of us in the United States are unfamiliar with many on this list – but honestly, this is where a lot of the growth and innovation is coming from. In the graph below, BCG shows that emerging market companies took a larger share of the market by growing at an average CAGR (2009-2014) of 13% vs. 4%. Also, operating margins have averaged 13%+ over that last 10 years. Who does not want a company that does 13% / 13%. 13% rev growth, 13% margin.

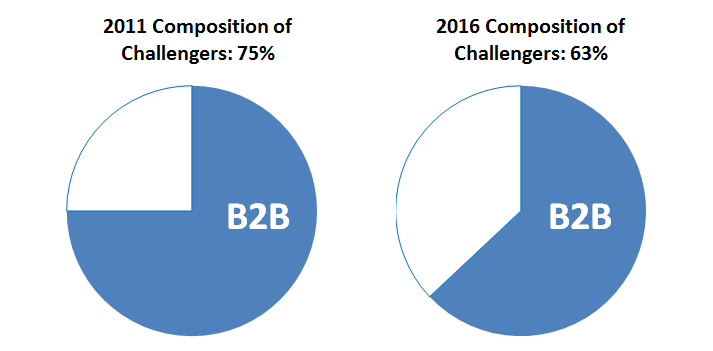

Lots of B2B companies

No surprise here. The majority of these companies operate in the B2B world where the supply chains are more global and more specifications-driven (not as sensitive to local designs, tastes, preferences). B2B composition of 75% in 2011, and 63% in 2016. (Side note: simple graphics are always better. BCG’s original graphic was colorful – but unnecessarily detailed and confusing. See here).

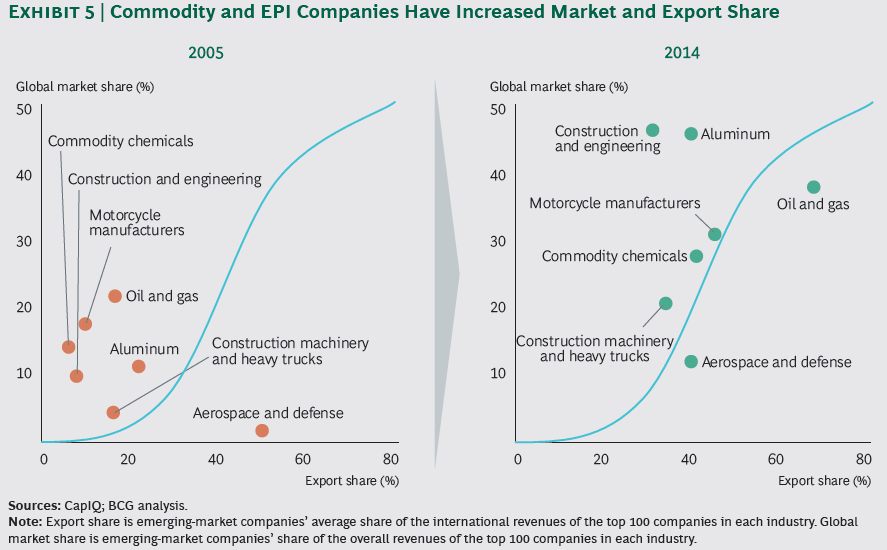

Heavy weighting in commodities, engineering and construction

Commodities have always been the domain of less developed markets (think: Asian spice routes, South African gold mines, Caribbean rum production, Brazilian forests) and a huge issue with development economics; poor countries sell their wares at low prices without processing and adding value – ergo – they get pennies on the dollar compared to the value of the end product. It’s certainly progressed since then, but look at the heavy weighting on the heavy industry side. . . market share from the 10-20% range to now 20-50% range. This must put the pressure on mature market companies like Foster Wheeler, Honda, Kawasaki, Dupont, 3M, John Deere, Manitowoc, US Steel. (Consulting tip, if you want to find the list of companies of a sector – like Steel or Iron – go to Finviz.com . . here)

Get the full list of 100 global challengers in the pdf, page 16/35 here.

From challenger to global leader

These challengers (top 100) have a great track record. Of the 193 that BCG identified over the last 10 years, 10% of them graduated to be global leaders. Looking at these names and their success:

- America Movil (Mexico): 3rd largest mobile provider globally, 43% of Latin America, operates in 45 countries

- Tata Motors (India): #2 largest bus maker, #4 truck maker; bought Jaguar and Land Rover, #1 in UK market

- Gazprom (Russia): #1 natural gas producer, expects 30% of revenue to come from Asia by 2025

Five attributes of global leaders

While it might seem a bit generic at first glance, BCG provides examples of why these attributes can transform challengers to a global leadership position. For me these are the most critical:

- Operating model – As Bain explains so well in Founder’s Mentality, there are many reasons why companies can’t scale

- Go-to-market – Let’s agree that data shows that 50%+ of M&A fail to deliver value. What works in 1 place, does not necessarily work half-way around the world. Business is beautiful in its complexity and nuances. Copy/paste does not work.

Competition everywhere

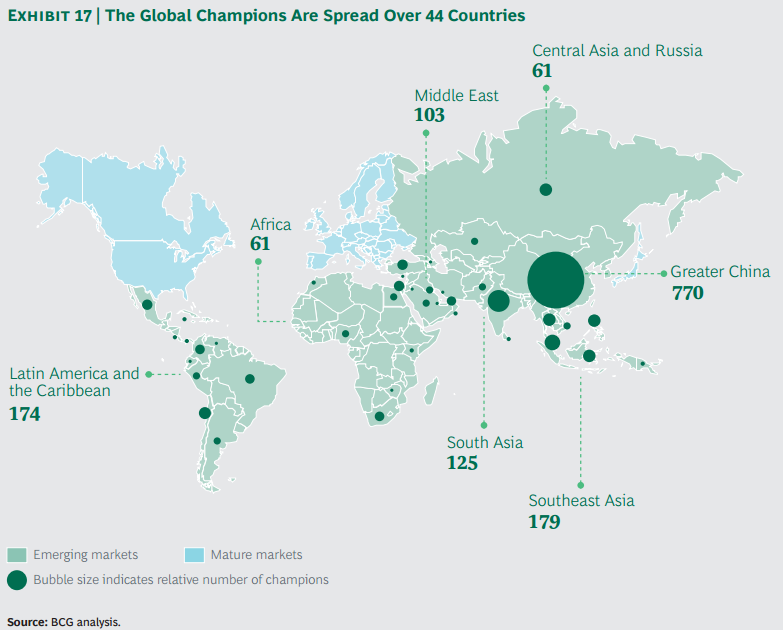

I am a big believer in free markets and competition; am encouraged by this report and how scrappy companies everywhere are giving big, incumbent multinationals a run for their money. For anyone who has read Friedman’s The World Is Flat (affiliate link), we know the competitive playing field is broad and flat. Look at this map if you need convincing.

As I wrote in a previous post, Whether you are a lion or a gazelle: when the sun comes up, you’d better be running.