The BCG 2017 M&A report has a great subtitle here (3Mb pdf) called the Technology Takeover. BCG notes that 30% of 2016 M&A involved the acquisition of technology companies (no surprise), of which 70% were from outside the technology sector (surprise). In sum, every industry is rapidly acquiring, morphing, and becoming technology companies. BCG goes one step further and buckets that 9 trends shaping technology M&A. As a consultant, gotta love this stuff.

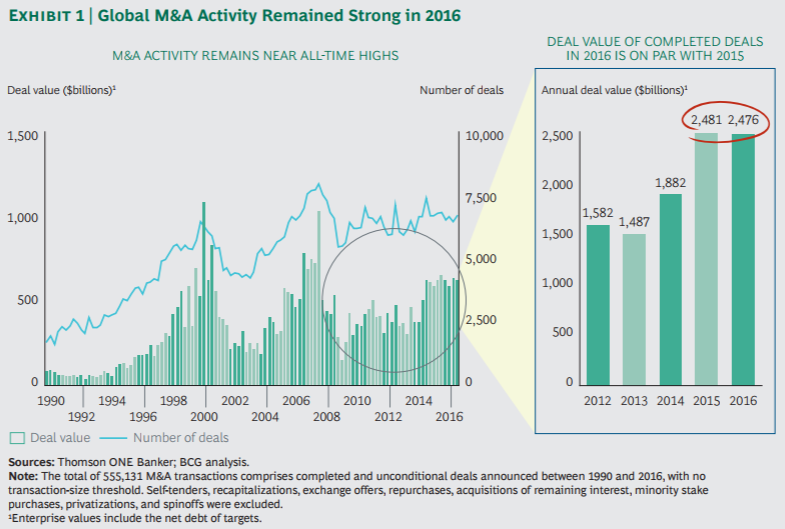

1. Global M&A still booming

In 2016, there were 26,000 deals totaling $2.5 Trillion (with a T), basically flat vs. 2015. Less than 1999 and 2007, but not by much.

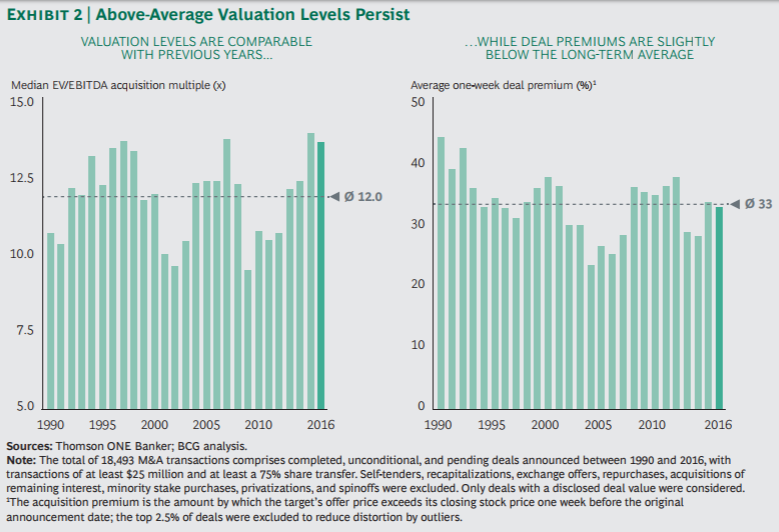

2. Valuations high

BCG notes that 2016 valuation of deals were 13.6 EV / EBITDA vs. the average of 12% (1990-2016). Clearly, this must be correlated to the higher-than-historical-average P/E in the US equity markets.

3. China outward M&A

BCG notes that Chinese firms doubled their outward (non-China) M&A by 100%+ to $200B in 2016. Side-note, this trend has been reversing over the last 10 months, as the WSJ notes here (Oct 2017) that Chinese outward M&A is down 27% YoY.

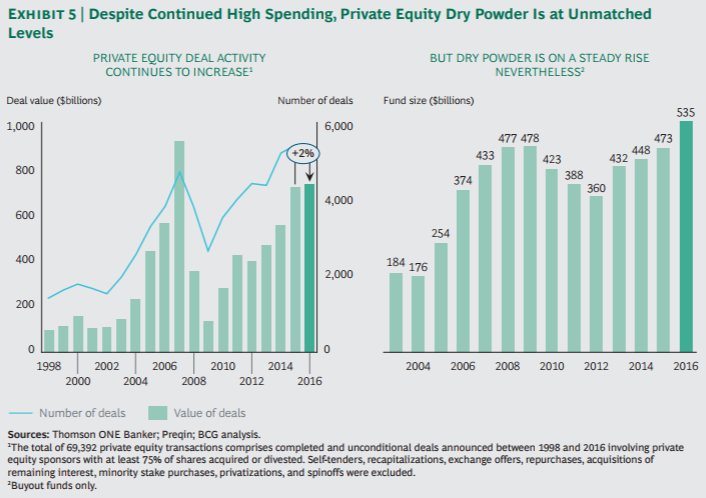

4. Private equity M&A continues

As you can see below, private equity M&A deals is essentially flat from last year (and near the all-time high in 2007), with lots of “dry powder” cash on hand to deploy into investments. Consistent with what Bain was saying about PE investments earlier this year.

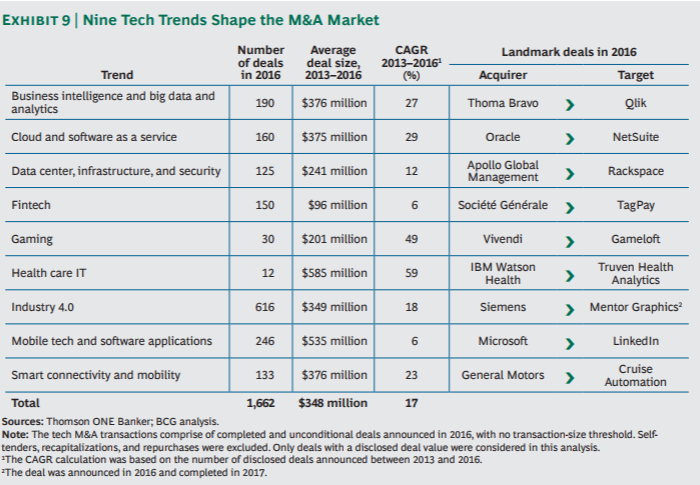

5. Technology is the story

This is the most unique analysis and shows consultants at their best. BCG took 1,600+ technology-related deals and put them into 9 buckets. Show the average deal size and the compound annual growth rate for last 4 years. Winning.

Big deals, lots of small deals

BCG made the hat-tip reference to Dickens and called this the “Tale of Two Market Places”:

- Big deals ($1 billion or more): 91 big deals made up 80% of the total value

- Small deals ($100 million or less) made up 80% of the volume of deals

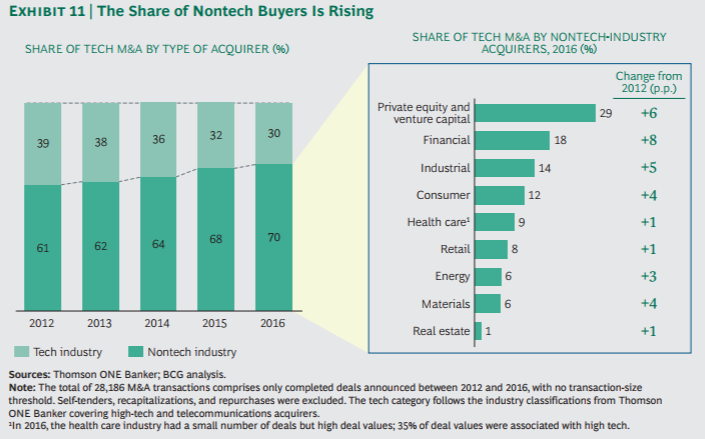

Lots of non-tech buyers

Looks like 70% of the total technology-related M&A deals were with non-technology buyers. Obviously, this is swayed a bit since private equity was the largest acquirer (and by definition non-tech). It’s fascinating nonetheless, as technology is not just a industry, but a means of innovation, customer engagement, cost reduction, and ultimately, value creation.

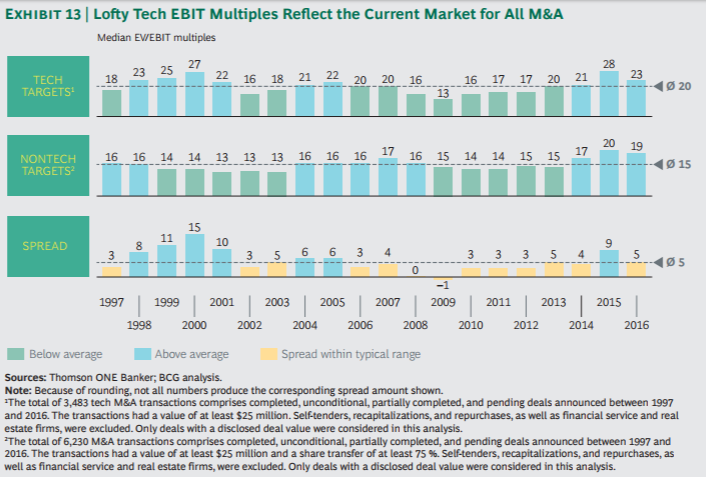

Comparing tech vs. non-tech valuations

Consultants love data, and BCG does a great job bifurcating (SAT word) deal valuations between tech and non-tech. Over the last twenty years, tech was at a median EV/EBITDA of 20, vs. non-tech of 15, as there is lots of cheap money and the markets seem to be rewarding growth.

Most deals fail to create value

Many longitudinal studies show that 1/2 – 2/3 of mergers and acquisitions fail to generate value. BCG’s study of technology M&A seems to agree with this grim assessment, scoring the tech deal space at 50-50. The final 15 pages of the report address the challenge of “Doing Tech Deals Right.” This likely deserves its own blog post and treatment, but for all those aspiring investment bankers, consultants, and M&A-minded people, it’s worth your read here.