Bain published a 2018 Private Equity report (80pg) which you have to sign up to get here. The high-level message seems to be that private equity is doing well (perhaps too well) and there is a lot of investor money looking for returns. This is driving up valuations for acquisitions, and honestly, making it more difficult for general partners (GP) to find bargains.

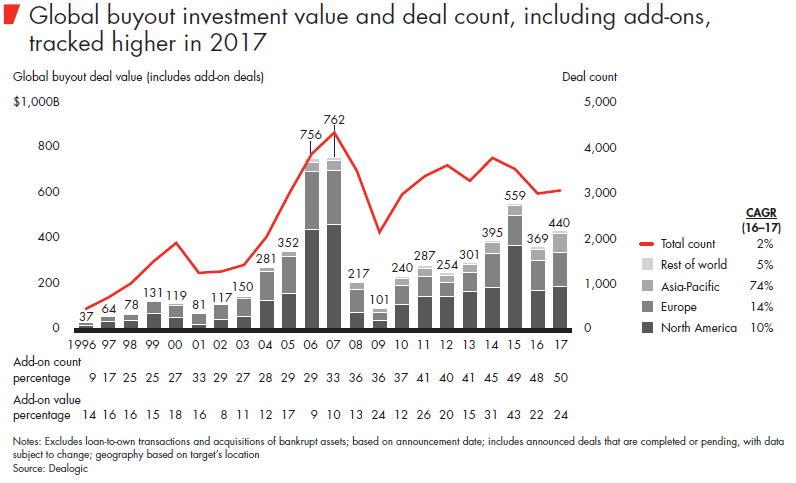

Number of PE deals flat in 2017, value up 19% to $440 billion

The number of deals (red line) looks flat at 2%, and the deal value is about $440 billion, lots of growth from Asia Pacific. In retrospect, look at what banner years 2006 and 2007 were, then the recent low was 2009. Since then, private equity has consistently been on a steady trend upward.

What’s an private equity “Add On” deal?

You’ll notice that the title of the graph says, “including add-ons” which I learned means tuck-in acquisitions. While these deals are smaller, they make up about half of the total number of deals. This allows PE firms to put together larger enterprises for “buy-and-build” approaches. Economies of scale still matter. This approach helps PE firms bulk up their investment: get more market share, stronger position, and hopefully, richer exit P/E multiple.

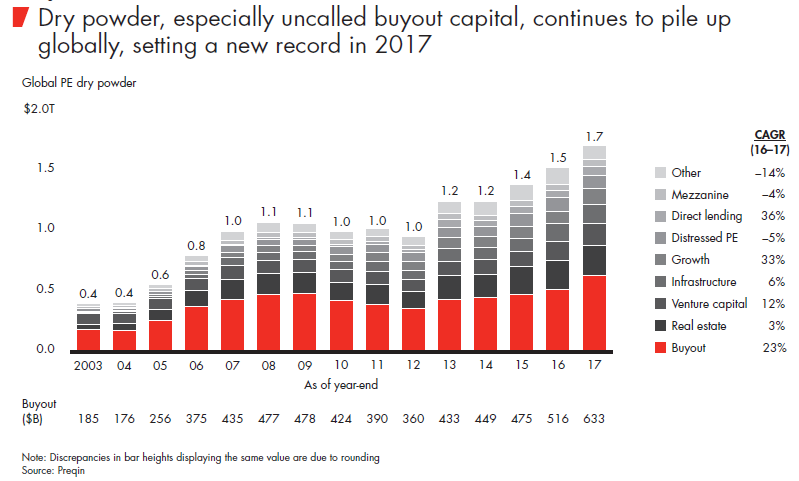

PE firms have $1.7 Trillion of “Dry Powder” to invest

Private equity continues to attract capital for a number of reasons. PE has offered great returns (in sharp contrast to hedge funds). Investors want to maintain, or increase their PE allocation. As a result, there is approximately $1.7 trillion in PE funds waiting to be invested.

Investors want more private equity

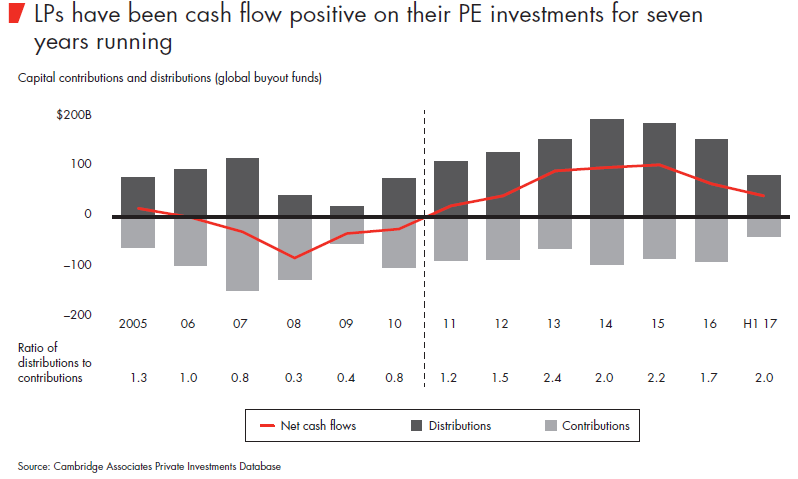

Private equity has provided an average return of 8.5% annually over the last 10 years vs. 4.2% for equities, which makes this crazy attractive to investors. Also, 92% of institutional investors want to maintain OR increase their PE allocation in the new year. Combine this with the fact that equities have been in a 10 year bull market, means that investors have $$ to invest and want more PE fund investments. Now look at this chart.

To the layman (read: me) this shows that PE firms have been net/net returning principal back to their shareholders. Yes, they get good returns. Yes, they are liquidating investments and returning principal back to their limited partners. On the surface that’s a good thing – get your money back. However, if you are a pension fund looking to maintain a 10% exposure to PE, getting your money back. . . is well. . . .not helping your allocation.

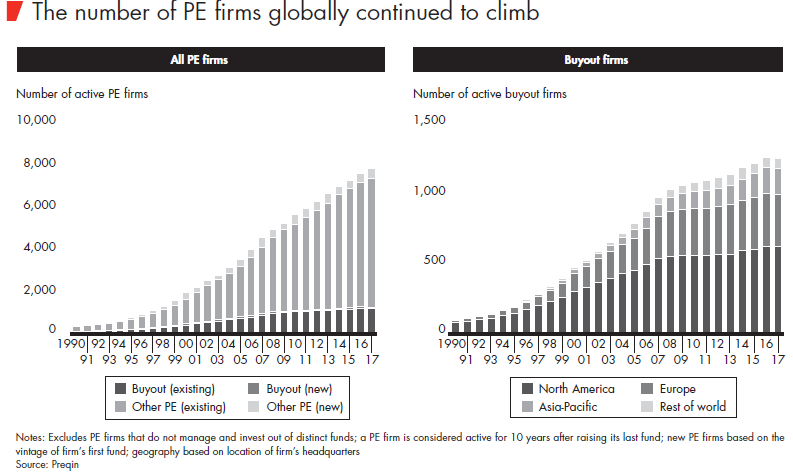

7,700+ private equity firms

The number of private equity firms keeps rising, with 1,300+ active buyout firms (defined as less than 10 years since raising their last fund). Bain notes that a lot of competition is actually coming from corporate strategic buyers – who are looking for inorganic growth, have a lower WACC, and are willing to pay for synergies.

Because GPs often lose out in head-to-head competition with corporate buyers (looking at standalone, or platform, assets only), private equity’s share of overall M&A activity globally declined in 2017 for the fourth year running.

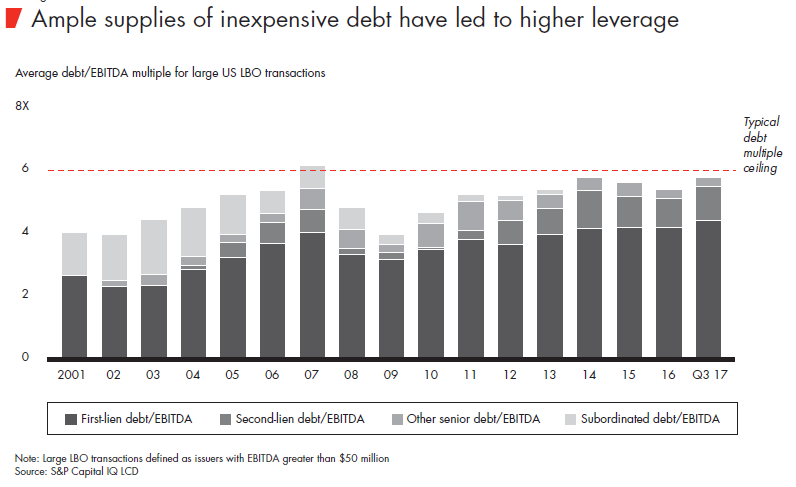

Low interest rates driving more debt financing (of course)

Money is still cheap with a 10 year at ~ 2.74% and private equity firms are boosting returns with lots of low-cost leverage. As Bain puts it, “The markets for speculative bonds and leveraged loans are as robust as they’ve ever been, as investors clamor for higher yields to augment their returns in a sustained low-interest-rate environment.” As a cautionary tale, the average debt / EBITDA multiple keeps creeping higher. How much debt is too much debt?

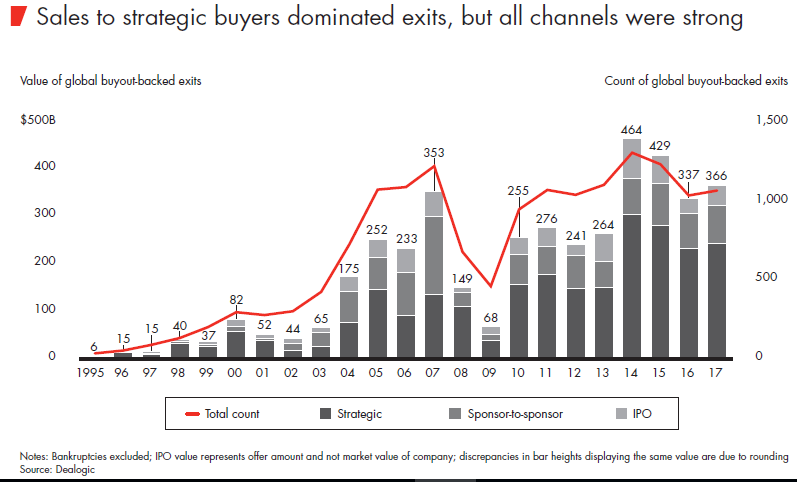

A seller’s market

The competition for good deals makes it difficult to find cheap deals, but makes it easier to sell. As you can see below, the sales to strategic buyers was by-far the largest portion of exits, followed by sponsor-to-sponsor exits (read: selling to other private equity funds). The smallest portion of exits was IPO; I found this interesting, as I (mistakenly) thought IPOs were the end-goal of all PE deals. Obviously not.

PE Trend #1: Lowering the minimum investment to $1 million

Historically, private equity was an exclusive investment category only available to limited partners able to dedicate $5 million+ to a longer-term investment. Now, Blackstone and others are looking to democratize this, allowing “Joe Main Street” to invest with as little as $1 million. Cheers to the little person.

PE Trend #2: Zombie funds?

The competitive environment is forcing private equity firms to get more aggressive, more creative, and more long-term. They are hunting larger prey, taking public firms private. Also, looking at sponsor-to-sponsor opportunities.

- Buying assets from other PE funds – Since PE funds often have a targeted 5 year holding period for investments, it’s smart to look for assets in other people’s portfolio which might go “on sale” within the next 1-2 years

- Zombie funds raised funds more a long time ago, and have not done a deal in the last 3 years. Naturally, PE firms are willing to take some of these companies / investments over.

PE Trend #3: “Carry” Is taxed as ordinary income if < 3 years old

With the new tax law change, any “carry” from investments held less than 3 years will be taxed as ordinary income, not capital gains. For the investment professionals, this is uncool. Small nuance (3 years vs. 1 year) is a big $$$$$$$ deal. Let’s see how this tax code tweak affects the average period of investments.

PE Trend #4: Who decides when to exit the investment?

I always thought that the partners who put a trade on, would be the ones to decide the exits. Finish what you start, right? Looks like that is increasingly NOT the case, as PE firms want to be disciplined on the exit strategy. Also, a surprising number of funds hold on to equity stakes in their firms to sell the rest out at a later (presumably) higher valuation.

In an effort to ensure that they are exiting companies at the optimal time and generating the best return, a growing number of GPs are taking the exit decision out of the hands of the managing directors who found and nurtured the deals.

PE Trend #5: economies of scale matter: mega funds of < $5 billion

As with many things in business, the big get bigger. The $24+ billion Apollo fund was the largest fund so far, and KKR’s $9+ billion fund the largest one dedicated to Asia Pacific. Megafunds over $5 billion accounted for 58% of total funds raised.

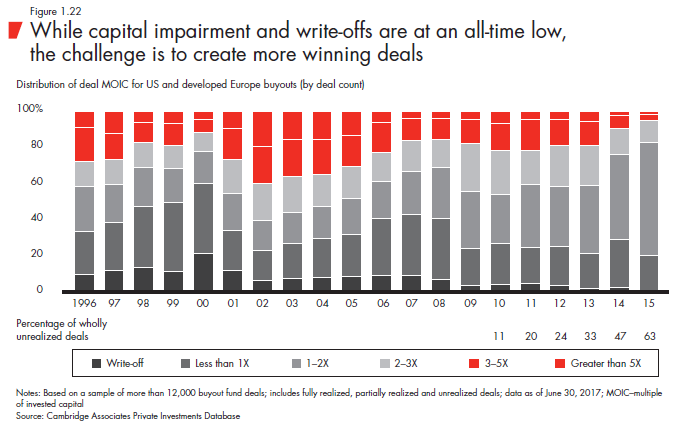

It’s all about the returns, silly

Private equity are incredibly good at what they do. Identifying undervalued assets, tightening operations, positioning firms for sustainable competitive advantage. Yes, losing deals (capital impairment and write-offs) are almost non-existent, but the home-runs (3-5x multiples of invested capital, shown in red) are also shrinking.

Worth Reading.

This blog post only covers only 1/2 of the report here. The rest of the report identifies ways for private equity firms to generate value from the inside out. Reads a lot like operations excellence and HR consulting, of which, of course, it is.

Related posts: