Consultants should be a quick study. Imagine that you find out on Friday afternoon that you are going to be staffed on a new project on Monday. You better spend 2-3 hours getting smart on the industry and company. To that effect, wanted to choose a random company and show how I might go about it. Imperfect, but hopefully helpful. To choose, I went to www.finviz.com and chose the first company in the alphabetical list. . .simple enough. . . A

Agilent Technologies

I don’t know much about the company other than it was the electronics testing division of HP which was spun off a long time ago. Also, there is an Agilent facility about 10 miles from my house, which I have passed by in Atlanta a few times. Don’t know anyone who works there. Okay, here we go.

Start with Finviz

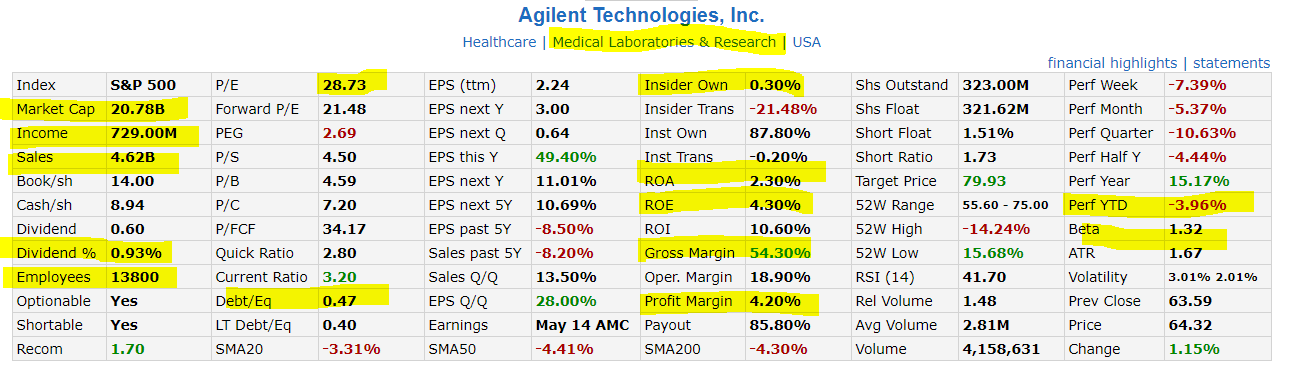

1) Go to www.finviz.com and find out the basic financial ratios for Agilent here.

- Medical lab and research industry? That’s not what I expected. . .

- Sales of $4B, with profits of $720M, not bad

- Market cap of $20B, could be a potential acquisition target ($billion is not what it used to be)

- Dividend of less than 1%, perhaps they are still growing, not giving much of a dividend

- Employees of 13,800, not small; simple math ($4B / 13,800 = 280K per employee)

- Debt / Equity of 0.47, so not very leveraged

- P/E of 28. . . kind of high, especially for a company with EPS growing at 10% or so. . .

- Net profit margin of 4%. . . yuk, this is not good, about the same as hospitals

- Beta (measure of risk compared to overall market) 1.32 (greater than market), not good; especially when the year-to-date performance is -4%

So from this initial cut, not so promising. Smallish company, low ROE, low profit margin.

Investor relations website

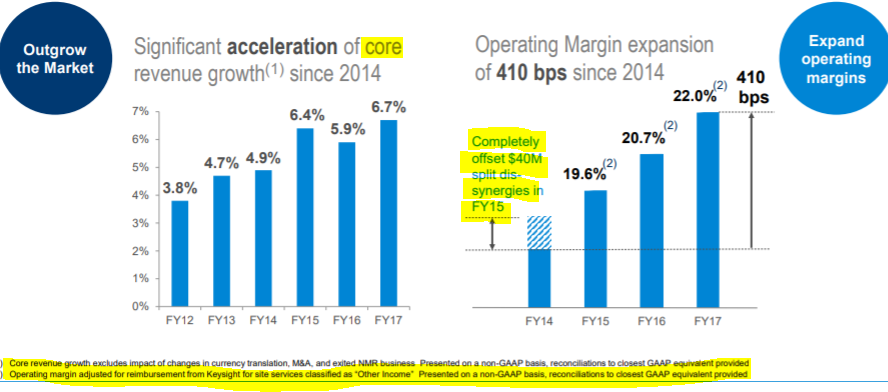

2) Go to the website, and look at their investor relations presentations. This is what they are telling their shareholders. This was their most recent presentation at a JPM conference (2018, no longer available). On the surface looks like revenue is growing (great news), but I highlighted a bunch of caveats. What is “core” revenue growth? What are all the footnotes?

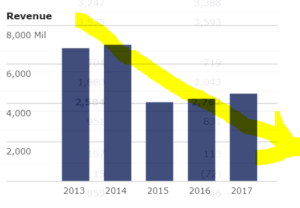

2a) Curious about “core” revenue, I went to Morningstar and saw a different revenue picture here. Not an investment banker, but the graph below looks pretty different from the one above. Hmm,

What is a huge drop in revenue from 2014 to 2015. Quick Wikipedia (yes, fastest way) search shows that the company split into two parts in 2015. NB: Any discussion of Agilent from 3 years ago needs to consider the combined company (A+KEYS). Gotta remember that they spun off part of their business in 2015. Now, they are 2 separately listed companies:

- A – Agilent is the life sciences, diagnostic lab company.

- KEYS – electronics testing and measurement company

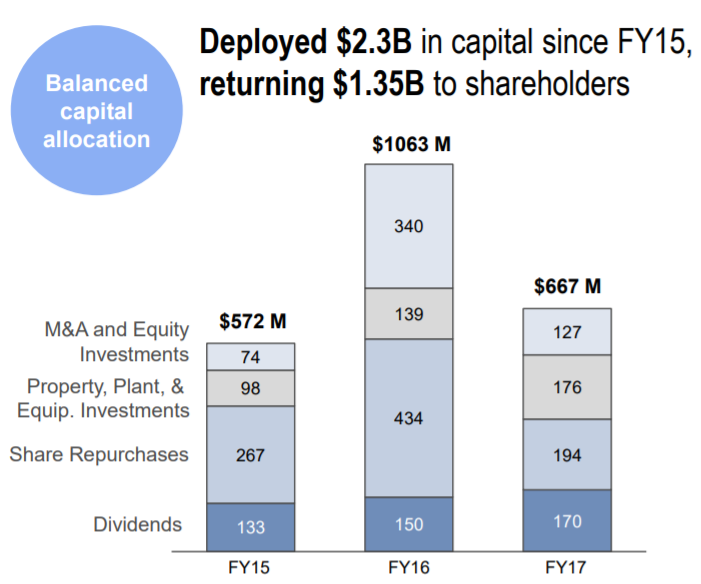

2b) In the IR presentation, they talk about how they are deploying their capital:

- Giving $1.3 billion back in dividends and stock repurchase. Good thing? Indicates potentially lower growth

- Acquired $500+ million in acquisitions over last three years (would be interested to talk with industry expert to get a sense if these were wise purchases, or they are just chasing growth at any cost)

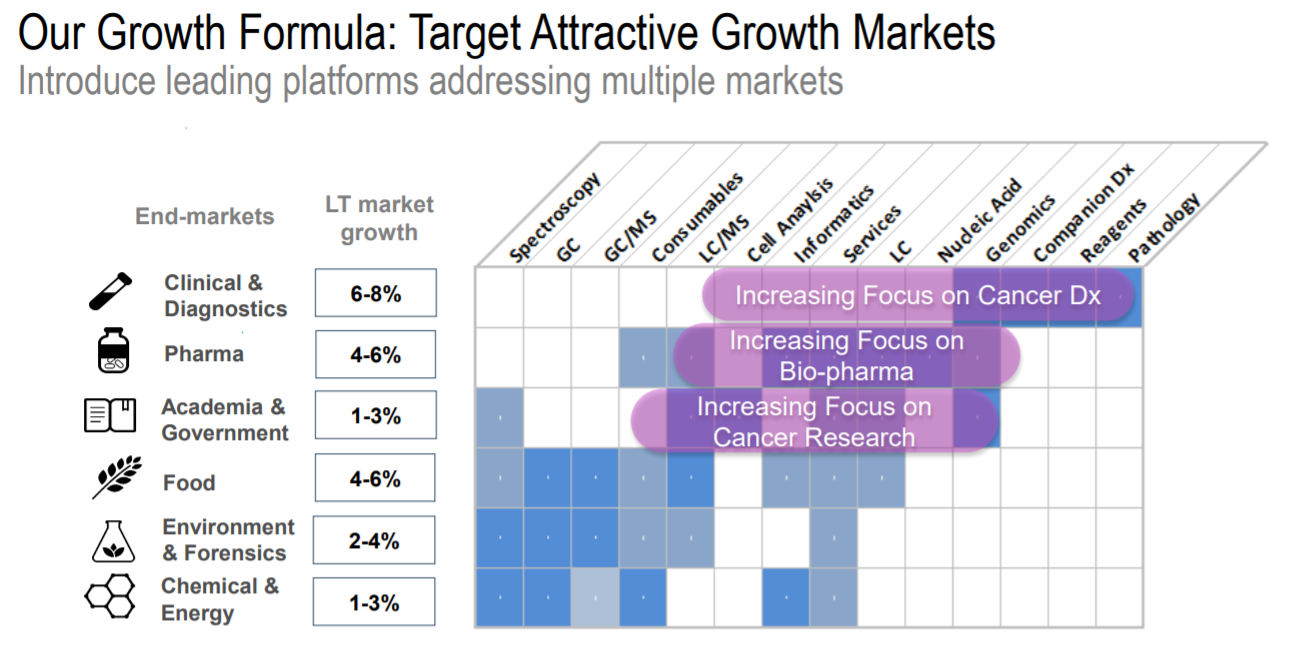

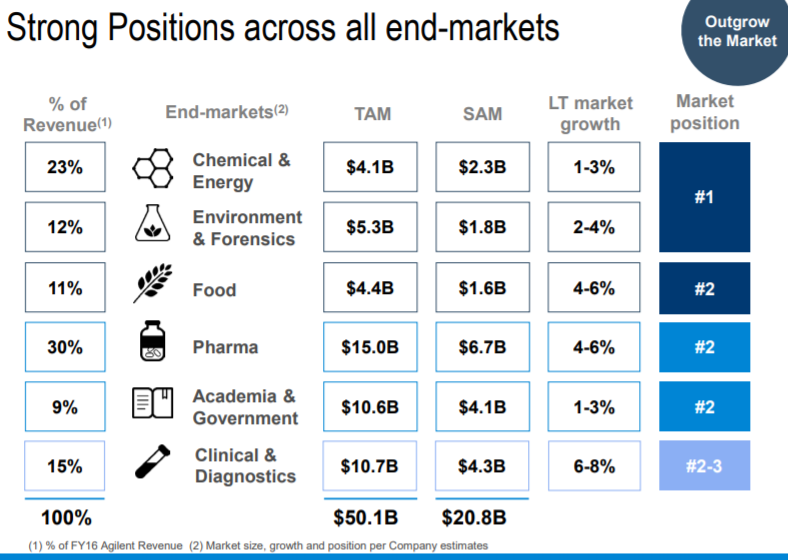

2c) This is their segments & targeted applications. As a consultant, love these tables. Helps you understand how they see the market, and what their plan will be. While this does not say exactly what the shaded blue colors mean, the purple seems to indicate their future growth (organic + M&A intention). This is when you call in your laboratory friend and ask their professional opinion.

2d) Looking at the same table 4 months prior (2018, no longer available) they show the composition of their business by segment and market position. All good stuff for a consultant looking to get smart on this topic.

Calculate DuPont Method ROE

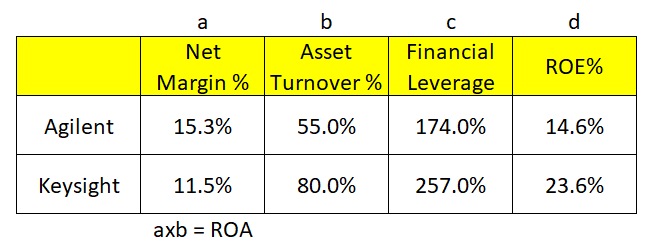

3) From here, I pretty much default into the DuPont formula. Yes, you should memorize this and use it frequently. I think Morningstar has the best website for this information

- ROE = Profit margin x Asset turnover x Leverage; also, ROE = ROA x leverage

- Looks like ROE for both post-spin-off companies (A & KEYS) is good 14-23%

- NB: High ROE is not always a good thing; can be easily manipulated etc. . .

- Net margin – pretty profitable business

- Asset turnover – slow asset turns. Thought that DGX (competitor might be better), but they are not. About same.

- KEYS has higher asset turnover (asset efficiency), and a LOT more leverage

Fill in qualitative information

4) From the ‘hard’ facts of the company, here I will start looking some of the executives, watch videos and start to get a sense for what the company is up-against. Key – what are their key challenges and what are the kind of problems they are looking to solve:

- YouTube videos of the management team

- Glassdoor reviews of working there

- Indeed.com job openings

- Quora questions and answers

4a) After watching a few short videos on Youtube, I am now of the opinion that DGX and LH are their customers, not their competitors. This dramatically changes my opinion on whether I should compare ROE etc. Some will argue that I should have done the Porter’s 5 Forces (industry / competitor) look earlier with the 10K. Completely agree. Your can <CTRL> + F and search “competitors:

- Danaher

- Perkin Elmer

- Shimadzu

- ThermoFisher Scientific

This is my 1 hour version of background research. What would you do differently?