(geek alert) The DuPont Method is one of my favorite things from B school. Yes, it’s a way to calculate return-on-equity, but it’s also a great way for a consultant to get smart on a company quickly. It’s a great first step in tearing apart financials and comparing companies from the same industry.

What’s return on equity (ROE)?

This is the first obvious question, and sadly, this yields a somewhat obvious reply. Return on equity (ROE) is well, your “return on equity” No mystery here. A = L + E. You have Equity (nice), so what is your return? The simple formula looks like this. ROE = net profit / shareholder equity. However, this is BORING, and does not help you understand WHY you are getting those returns. For example, two grocers (Kroger & Sprouts Farmers Market) have the same ROE of 27%, but their businesses are quite different. . .

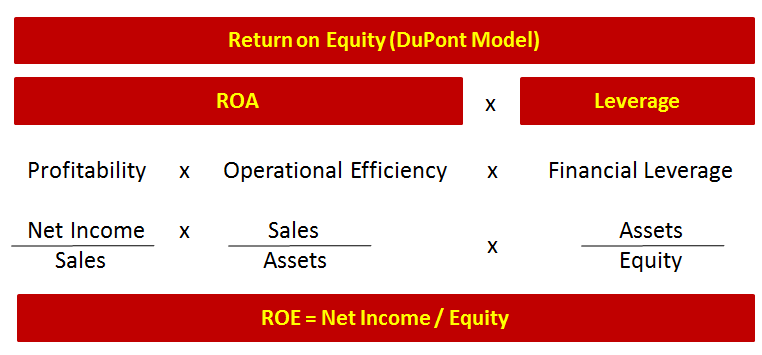

Du Pont Method = ROE = profitability x asset efficiency x leverage

The Du Pont formula (or method) is better because it breaks ROE into three different parts. It was crafted by the folks at Du Pont in the 1920s, and while it might feel longer (3 parts instead of 1), it’s better. Trust me.

- Profitability (are they making money on each sale?)

- Asset efficiency (are they selling enough stuff?)

- Leverage (how much debt are they using to get returns?)

It’s super winning because it is a 3-for-1 special; tells you something about a company’s profitability, asset efficiency and leverage. You get a little bit of income statement + balance sheet, all rolled-up in one ratio. What’s not to like? The full version has 3 parts. . . which elegantly cancel each other out (red font).

ROE = (net profits / sales) x (sales / average total assets) x (average total assets / shareholder equity)

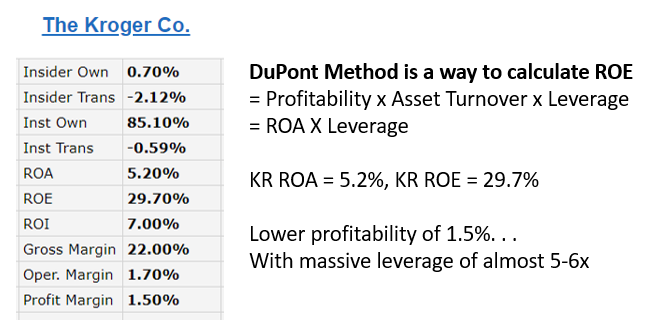

Kroger (2,700+ stores, $122B in revenue) 27% ROE

Let’s look at Kroger grocery stores. You can look up KR on Finviz here, and you see that they have super low margins of 1.5% and super high leverage of 5-6x. Note Finviz uses a 5 year average for net margin.

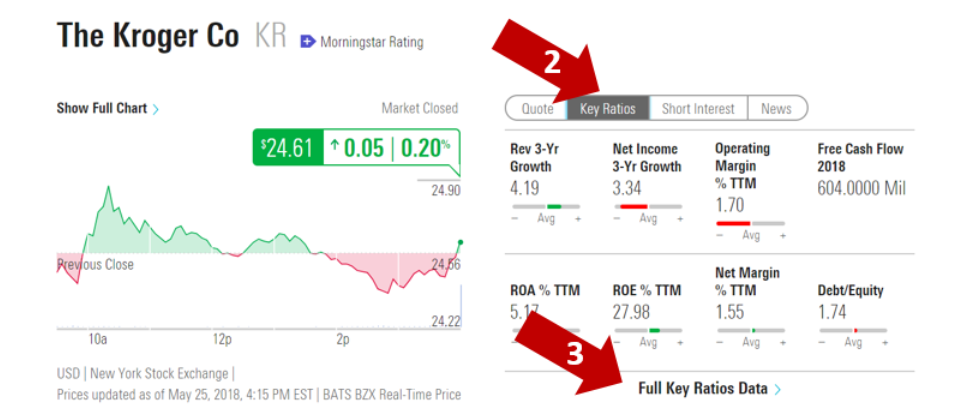

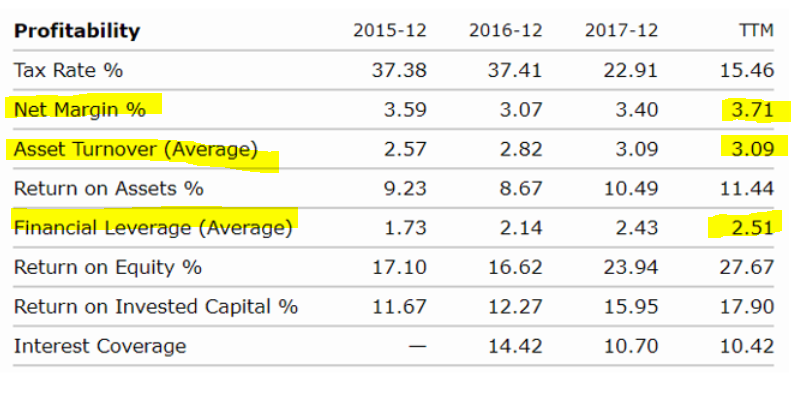

For DuPont Method, Morningstar.com is a better way to go. It gives you all three elements separately. Step 1) Type in ticker symbol into the . 2) Click on KEY RATIOS, then click FULL KEY FINANCIAL RATIOS, or click here.

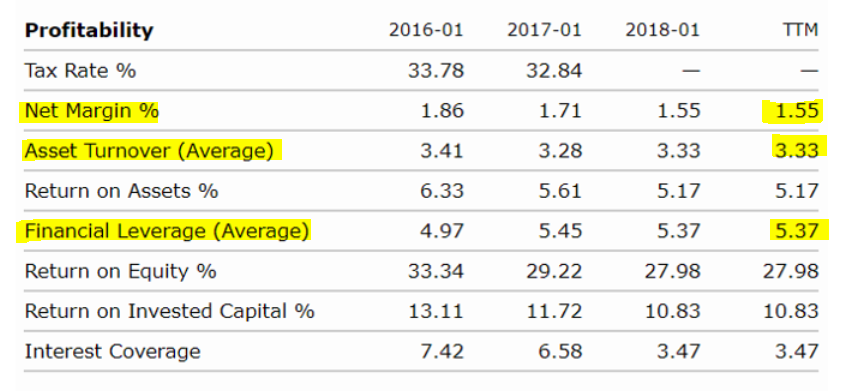

From here, you will see a huge list of financial ratios, but scroll down to this section called profitability. You can see all the ingredients needed for our Du Pont Method cake-baking. Like we saw on Finviz, KR ROE is in the 27% range. Using TTM (trailing 12 months).

- Profitability is 1.55% (not great)

- Asset efficiency is 3.3x (pretty good)

- Leverage is 5.37 (kinda scary)

So in high-school English, Kroger sells a LOT of stuff, at almost no profit, and borrows a lot of debt to do it. You can also do the back-of-the-envelope math and see that ROA (5.17) = profitability (1.55) x asset turnover (3.33)

Sprouts Farmer Market (300 stores, $4.8B in revenue): 27% ROE

Curiosity = a good thing. Let’s look at another grocer – Sprouts Farmer Market (SFM) here.

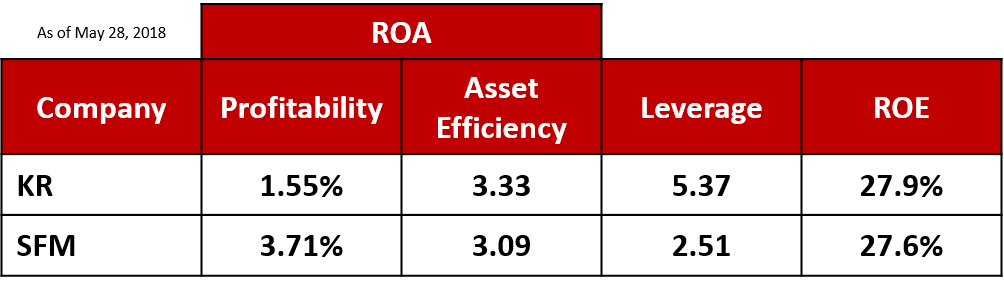

When you put it all together in a table, it looks like this:

- SFM is a lot more profitable that Kroger (think premium products, segmentation into bourgeois neighborhoods)

- SFM asset turnover is good. Not as good at KR, but has improved alot. . they were 2.57 in 2016.

- Leverage is a big difference here. KR has 2x the leverage (read: borrowing money from banks and bond holders)

This is just scratching the surface. This is why consulting (and business more generally) is fun. It’s a big detective hunt. From this initial Du Pont analysis, my mind starts to ask many more questions:

Profitability

- Are they both ONLY in grocery? What else do that do? (e.g., Kroger also owns jewelry stores, gas stations)

- What is the product mix for SFM vs. Kroger? What’s profitable, what’s not?

- With 5-to-1 leverage, any jump in profitability will be a huge boost to KR. How to increase margins 30-50bp?

Asset Efficiency

- With Kroger’s size, there should be economies of scale. What is best asset turnover in the grocery business?

- What are the assets that KR and SFM own? If the outsource anything, it’s not an apples-to-apples comparison.

- What is the square footage of SFM vs. Kroger stores? SFM has 1/10 of the stores, but a lot less than 1/10 of the revenues?

Leverage

- Is 5-6x high or low for the grocery business? Yes, grocers have steady cash flows, but how much debt is too much debt?

- What is KR liquidity ratio? With that much debt, can they pay back their current bills?

So What?

The Du Pont method may seem long-winded (3 steps instead of 1), but it helps to tease out the root causes of ROE. One example I use in class is Tiffany’s and Walmart, which both have ROE around 13-15%. Those two companies are as different as Stark and Lannister.

Very Interesting analysis. Would love to see you build upon this and do further analysis

Thanks for reading. Yes, will be out of pocket for a few weeks, but can do more of this type of work. Super useful.

As much as I’ve always liked the Dupont Ratio, I’ve never liked it for mid-sized professional services firms where most of last year’s equity is paid out and the bulk of assets is in AR.

Do you ever tweak for professional services?

Mark, that is such a good question. Have to think on that. In the DuPont method, profitability will be the same for mid-size professional business, that part is consistent. For asset efficiency, there needs to be a way to translate human capital (i.e., people) into assets that are generating revenue. It’s much more than AR, desks, office space. So need to think about how to make the perilous jump from financial accounting to people are assets (not just expenses). Also, for the leverage of the business, if last-year’s equity keeps getting paid out, the next question is how much debt is getting taken on. David Maister did a great bit on this in his book, Managing a Professional Services Firm, let me dig that up . . .