PWC 22nd Annual Global CEO Survey here (48pg, 1.6Mb)

Reality check

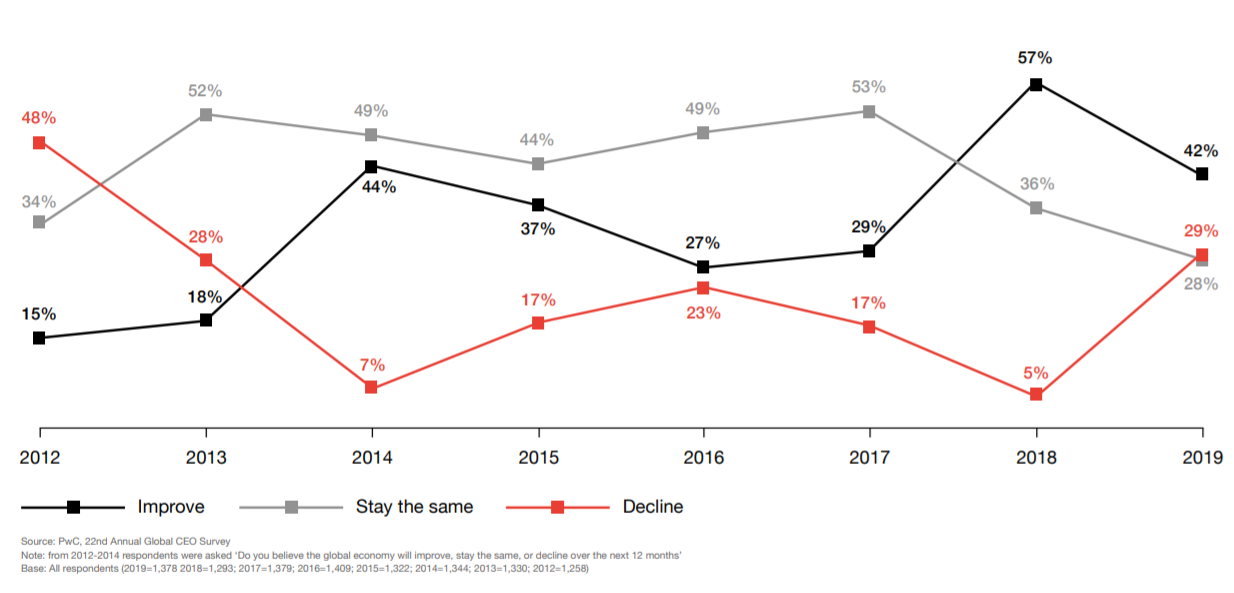

Last year, CEOs were optimistic. In contrast – for 2019 – 30% of CEOs are projecting a decline in global economic growth, up from only 5% last year. With all the bantering on tariffs, and trade restrictions, that is not surprising. The following chart shows CEO’s response to the question: “Do you believe global economic growth will improve, stay the same, or decline over the next 12 months?” A few takeaways:

- More CEOs think that the economy will improve (42%, black line) vs worsen (29%, red line)

- However, the red line (economy getting worse) is a lot higher than it was last year

- The trifecta of obstacles seem to be international trade tensions, political uncertainty, and fiscal tightening. In high-school talk (trade war, politics, and higher interest rates)

Looking inside-out for growth

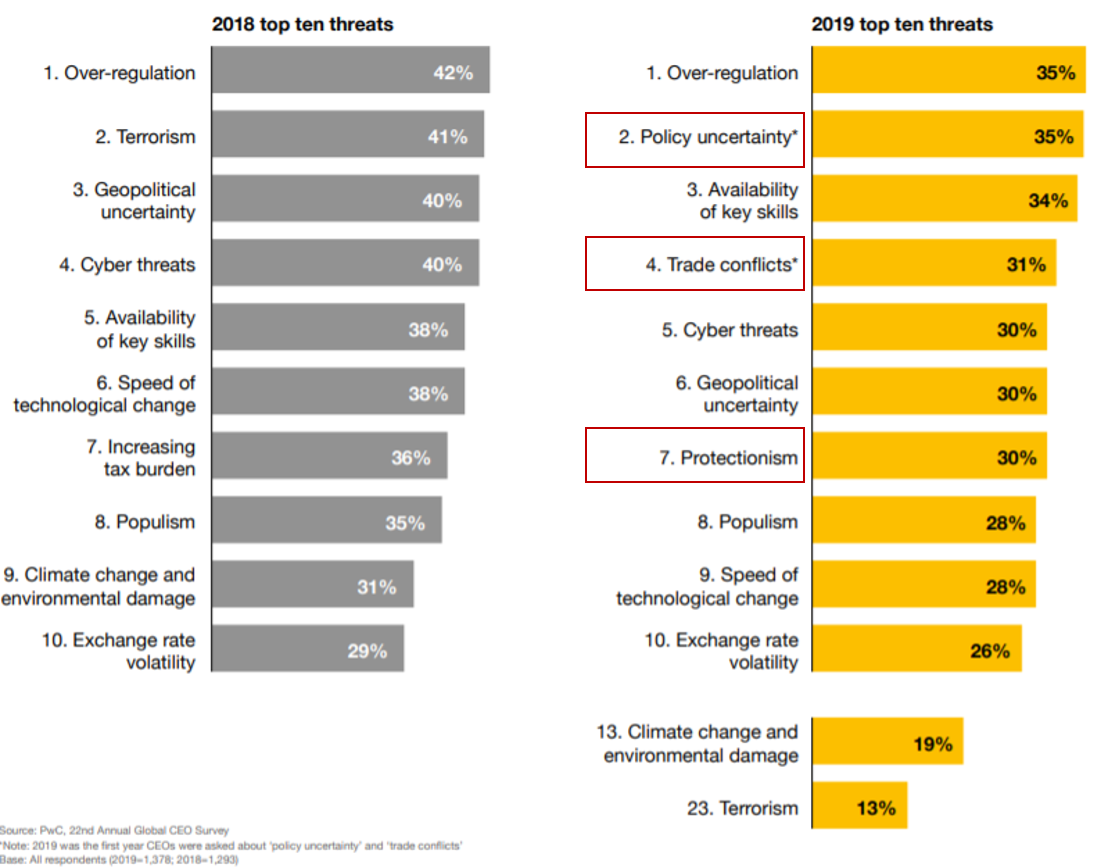

PWC asked CEOs what they perceived as the greatest threats to their business. MBAs – think of the PESTEL framework, Political, Economic, Social, Technological, Environmental, Legal. These are the responses from 2018 and 2019. A few things I saw immediately:

- There are a few new top 10 threats: policy uncertainty, trade conflicts, and protectionism (#2, #4, and #7 on the right hand side). Not to get too University of Chicago about it, but those are all self-inflicted by the government.

- The “availability of key skills” is top 3. This should be encouraging for continuous learners, for the intellectually curious, for those crunching Cousera courses at night, on topics unrelated to their majors. As Thomas Friedman might say, those who “dance in the eye of the hurricane.”

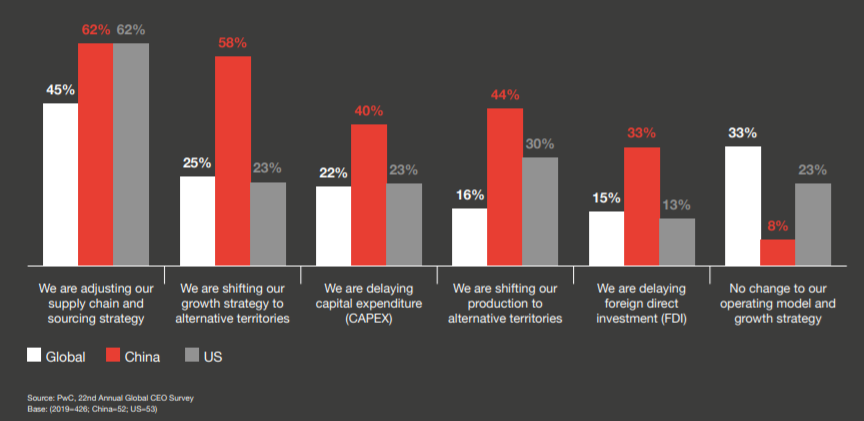

Massive irony: US and China CEOs have the same problem. They need to find ways to work around/through the government-imposed barriers to trade. In many ways, they are using the same approaches and equally suffering through the results. Macroeconomic policy via populism = lost productivity.

- Both US and China are adjusting their supply chain and sourcing approach.

- China is shifting growth to other countries (end markets).

- China is shifting production to other countries (of course) to shuffle step trade barriers, re-assemble, then re-export to the US. FoxConn said that would / could shift production to non-China based factories quickly. National boundaries are a fairly non-descript way to characterize trade, yes?

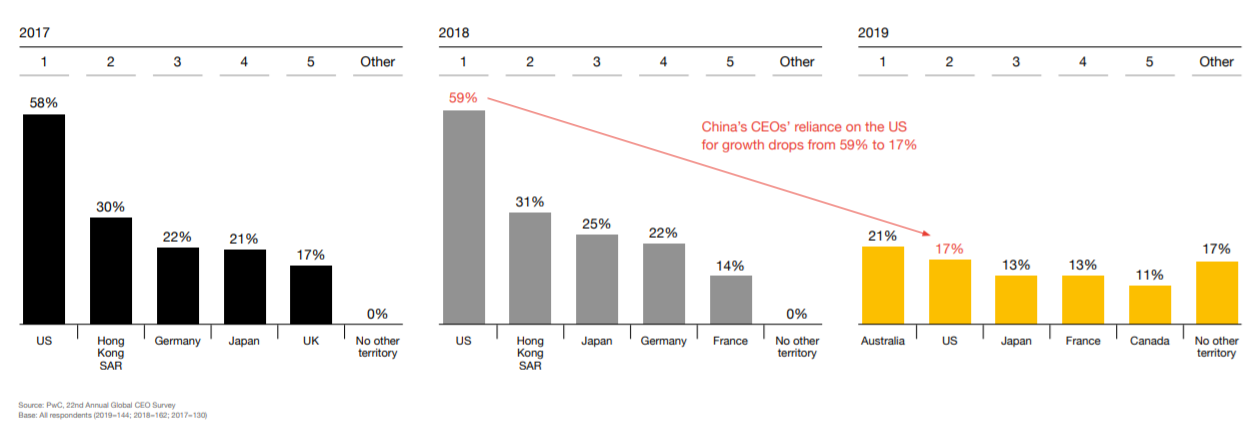

No surprise, China CEOs are de-emphasizing the US as an end-market for their products. In the graph below, China CEOs place the US market as #2 most important for their next 12 months, behind Australia.

Is this what US policy makers were envisioning? Winning?

Mind the information and skills gap

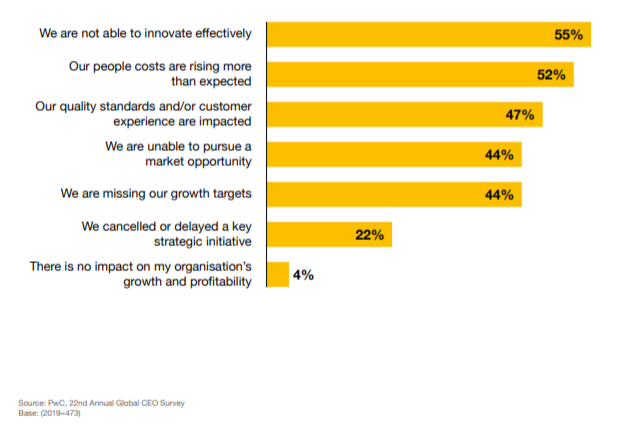

CEOs lament the gap between the human skills to harness the insights from the big data, and “deluge” of information coming at decision makers. When asked about the availability of key skills in the organization, this was their responses:

- 55% said their organizations are not able to innovate effectively

- 52% said their people costs are rising more than expected

This reminds me of the founder’s mentality study from Bain & Company, where they also discovered that CEOs cited internal obstacles as the primary reasons for not meeting revenue and growth targets. Too often, its the internal capabilities that are lacking.

“We just hired some very impressive data analysts to form a center of excellence, so I asked my recruitment team, “What was the pitch that you gave them to join us?” The single most important reason they joined us — some from much bigger companies — is that we bring them close to the customer on Day One. They’re not one of many, just working on algorithms. They’re with the customers, understanding their problems, and then designing solutions. They get a lot of satisfaction from that.” NANCY MCKINSTRY CEO AND CHAIR, WOLTERS KLUWER

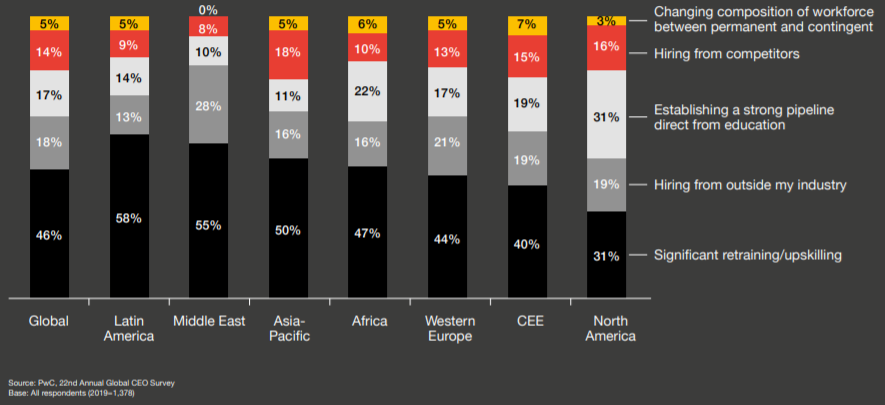

I found the following chart encouraging. When asked about the different ways to close the skills gaps, 31% of the North America CEOs talked about developing direct ties with education. This is what Thomas Friedman also talks about. . . the collaboration needed between government, non-profit, education, corporations, and the larger community. Yes, individuals need to take more ownership of their own marketability, and yes, corporations need to invest in long-term R&D to develop the human capital they need. Yes, and Yes.

Feeding the AI Engine

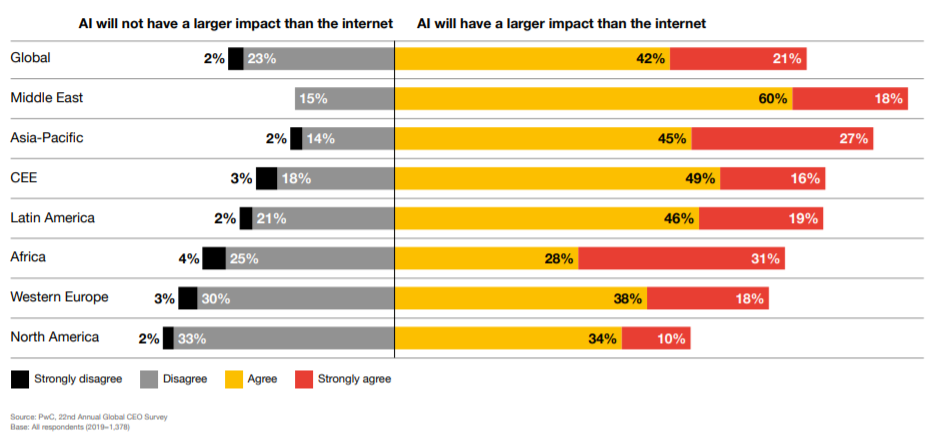

In the survey, 85% of the CEOs agreed that artificial intelligence would dramatically change their business in the next 5 years. Really like this provocative question that they asked: “How strongly do you agree/disagree that AI will have a larger impact on the world than the internet revolution?”

- Globally, 2/3 of the CEOs said that AI would have a larger impact than the internet (wha?)

- North American CEOs were the ones who most disagreed

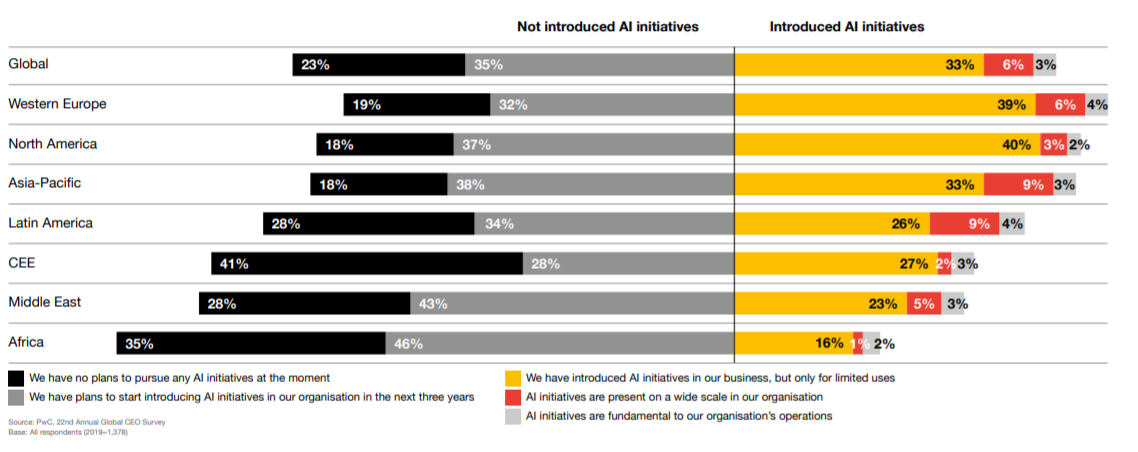

Despite this enthusiasm, 58% of CEOs have not introduced AI initiatives at all. . . and only 9% of companies implementing them at scale. This is not surprising now, but then again, I believe we will surprised at how quickly this chart becomes less Black and much more Yellow in the next 2-3 years.

We are now moving into the world of anticipative computing. We’re not only gathering data in real time, but also anticipating the data to come. You can tell what’s likely to happen in the next 30 seconds. And if you can predict it in that time, that’s all the time you need to prevent it or make use of it.”

NATARAJAN CHANDRASEKARAN, CHAIRMAN, TATA SONS

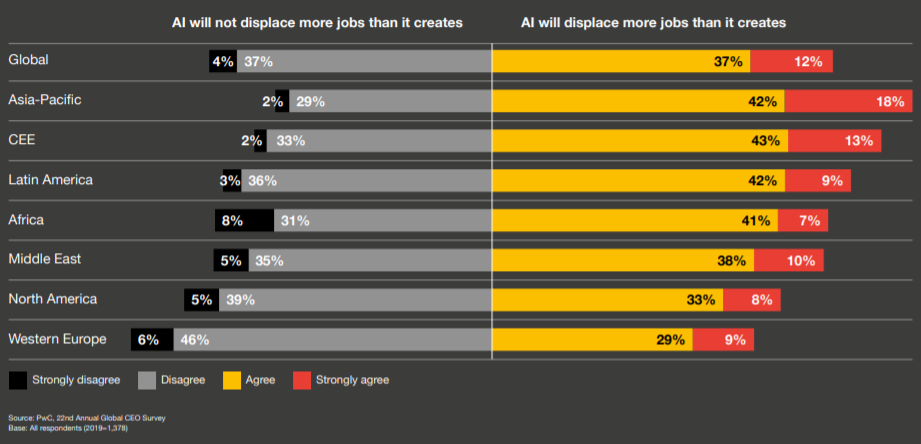

CEOs are divided on how much net job creation/destruction that AI will create. For me, the question is a bit flawed because the job that AI displaces and the job that it creates are very different in nature, location, value-add, and constituency. Are we just saying accounts payables clerk = data scientist?

Great survey, great sample size

We know that making good surveys is difficult. The folks at PWC deserve a lot of credit.

- This is the 22nd global survey – it’s tough work to be that consistent

- They interviewed 1,300+ CEOS;10% by phone, 17% face-to-face, and 73% by online survey

- 48% of them were CEOS of $1billion+ in revenue companies

- 59% were privately held corporations

Please download the original pdf here. Also, see their interviews with CEOs here.

Thx John, great work, as you always do!

thanks for reading