Happy 4th of July weekend. The country’s birthday makes me reflect on a lot of things – history, freedom, national governance, community, the future, and money. What? Money? Really John? Let’s not ruin the BBQ. Yep, money, let me explain why. . .

America = opportunity, right?

I am a huge believer in the US. I have HUGE expectations about our collective future. In my mind, the US was always the “new country”, the “melting pot” which was focused on tomorrow, not yesterday. America = opportunity. The problem comes when the US – both as a country, and as individuals – are so indebted that, well, we’re in trouble.

America was never perfect (trust me: read Zinn’s A People’s History of America (affiliate link), if you have doubts), but we were always pushing to change, reform, improve, and win. However, financially – we are not setting ourselves up for success. The US government has too much debt. Americans have too much debt.

What we call the States

When I was growing up, we learned a lot of names for the US. See a few of them in blue, and some of the questions we – as Americans – need to ask ourselves about our collective economic future.

- Land of Liberty – Liberty is about choices. What are some fiscal choices we need to make?

- Land of the Stars and Stripes – Does it make sense that our debt is a wartime levels?

- Union – What do we all NEED (All Americans), which takes precedence of a some peoples’ WANT?

- Land of the Free – How free are we when our federal debt burden is $70K per person?

- Home of the Brave – What are some scary sacrifices we need to make now on behalf of future generations?

Yes, the national debt can be a heavy topic. I know, so I found a cartoon to lighten the mood. This will help.

Great Minds Think: A New Guide to Money

This is the title of a 20pg free PDF that I discovered online here. It’s a simple cartoon workbook from the Federal Reserve Bank of Cleveland that aims to educate middle schoolers on money. It’s simple, direct, and useful.

Many folks reading this blog are financially savvy; you work in finance, trade stocks, know the difference between beta & alpha. So why talk about money like a 13 year old? Why? Because in the US – we need this:

- We, Americans, overspend

- Our government overspends

- We have forgotten the basics of money

The economy is in bad shape

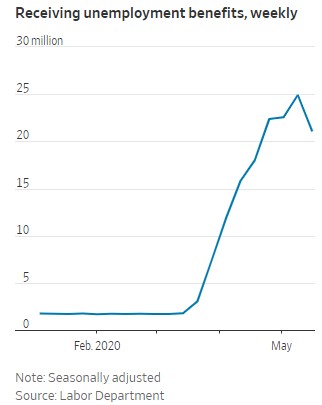

Covid-19 has been a menace to public health. Additionally, it’s a menace to the economy. It’s actually hard for Wall Street analysts to say smart things because the global economy has never been in a multi-month coma before. Airplanes are grounded, hotels are empty. Restaurants (with high fixed costs) can only safely operate at 30% capacity. Mauvais. Tres mauvais. Without being hyperbolic, this graphs says a lot:

Americans were already vulnerable

So, here’s the issue. Even before this economic winter hit, Americans were acting more like grasshoppers than ants. After the 2008 financial crisis, it was a pretty amazing economic run for 10 years: low unemployment, low interest rates, good stock market. It was great times, and yet as individuals:

- 44% of Americans had “expenses exceeding income” (MarketWatch, 11/2018)

- 62% of Americans had “less than $1,000 of savings“ (MarketWatch, 12/2015)

You don’t have to be a wizard to know that a) if you spend more than you make, then b) you’re not going to have savings. Hmm, not a good set up for the “average” American. . . Maybe nationally, we’re doing better?

US government = not fiscally prudent

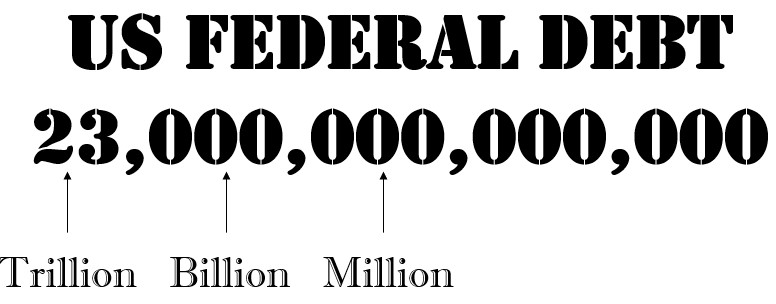

Nope, this is a dead-end. The US federal government is a terrible example of fiscal prudence. Just to be clear, Republicans and Democrats BOTH like to spend money they don’t have. They just spend it on different things. The federal debt is about $23 Trillion. Trillion with a T. Can we agree that’s a lot of money? It’s the equivalent to:

- $179,000 per U.S. household or;

- $70,000 per person or;

- Same amount as the economies of China, Japan, and Germany — combined

- Uh, it’s 23 Million, millions

Money = we all need to go “Back to Basics”

Maybe it’s time for some Benjamin Franklin-type common sense about money. This workbook is SO basic, and yet so good. It’s what we all need to review, middle-school-style:

Chapter #1: Choices

Absolutely love how this starts off. Choices. First three sentences say so much about economics and life:

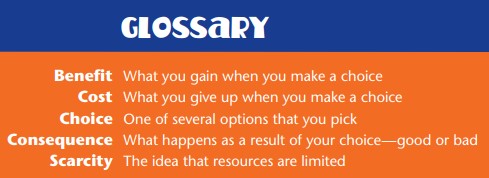

We have a limited amount of money that we can use to buy the things we need or want. This is called scarcity. Because money is scarce, we have to make choices about how to earn it, spend it, save it, or give it away.

Boom. Listen up everyone (yes, you too – Federal Reserve, Treasury, Congress). Money is not endless. There is a limited amount of money. “This is called scarcity.” Every decision has a cost, benefit, and a consequence.

Choices have a lot to do with values and willingness to forgo immediate gratification. Dave Ramsey often says, “Live like no one else (sacrifice today), so that you can live like no one else (financial freedom) later.”

If you have a high-interest rate student loan, a question you might want to ask yourself: Am I willing to NOT go out to eat 2-3 times a week, if it helps me to pay off my loan faster? If not, then we’ve already got a bit of a problem – and haven’t even started talking numbers yet.

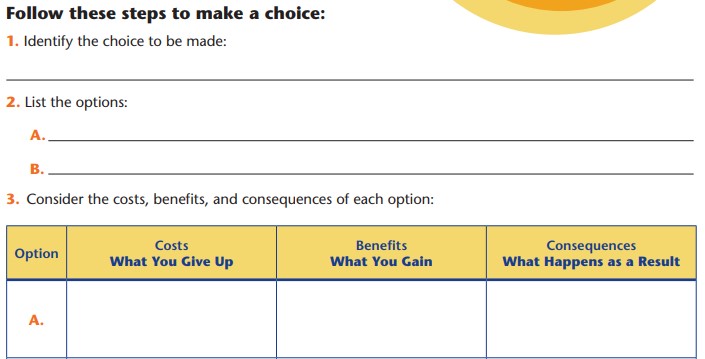

Costs, Benefits, Consequences

In true workbook fashion, there as multiple “okay, you try” places to fill-in-the-blank. Here, you make a choice, list the options, and more importantly, list the costs, benefits, and consequences. Note: Let’s be wary of politicians (or lobbyists) who don’t give a full picture. They mislead us by only highlighting the benefits, while ignoring the costs / consequences.

However simplistic this table looks, I’d argue that this approach is an evaluation matrix. As consultants, we create these on almost every project. It can be a decision matrix for:

- Investment criteria for different capital projects

- Vendor selection criteria for strategic sourcing

- Recruiting evaluation form to choose among candidates

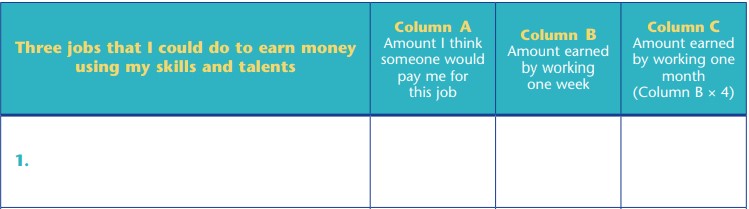

Chapter #2: Earning and Saving

Yes, start at the revenue line. Make money. For the US government this is tax revenue. For individuals, this is your business, pay check, or investments. College freshmen: think of this now – before you become a second semester senior. Remember: studies show that your salary after graduation is highly correlated to your major. Kinda makes sense. Computer engineering at XYZ Tech (usually) > sociology degree from Ivy League.

Consultants, this worksheet means project bill rate x project hours.

Savings rate = near zero %

Okay, my only complaint is how we are slightly misguiding these teenagers on savings. They talk a good bit about the difference between a checking vs. savings accounts, but with the near-zero interest rate environment, this point is moot. Looks like you can get 1% on a 1 year CD. Money in the bank is dead money, right now. Perhaps there needs to be a sequel workbook on investing. . .

Chapter #3: Spending

Of course, it’d be easier to just tell people to not spend. Save, save, save. However, this approach is smarter because it teaches two core concepts to middle-schoolers:

- Needs vs. wants (not the same thing)

- Opportunity cost (what? every choice has a cost?)

Needs vs. wants

Sheesh, this is important, and yet, we adults mix this up all the time. We falsely think everything is urgent, everything is required, everything is relevant. No discernment. Just insatiable, impatient desire. No bueno.

It’s something we all need to work on. What’s important vs. what’s nice? For example, as an individual buying a home: what’s critical (school district, taxes, size, location) vs. nice to have (crown molding, walk-in pantry)? Unless you are able to prioritize, you’re going to be frustrated chasing down a random list of things.

This grid forces you to put the items into columns. . .NEED or WANT. Also, NEED how much (1-5) and WANT (1-5). Even the most savvy executives sometimes conflate a NEED and a WANT. This discipline is so important.

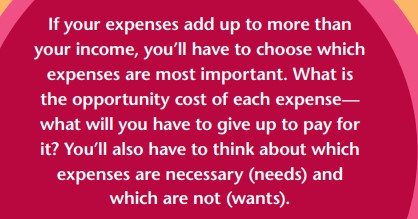

Opportunity costs

For anyone in professional services – attorneys, consultants, marketers, bankers – we need to continually think about how we spend our time. If you have a “bill rate”, then time is money. Value your time. If I were not doing X, what else could I be doing? Same holds true for your resources.

When you choose to spend your time or money on one thing, you give up the opportunity to spend it on another thing. The other thing that you give up—your second-best choice—is called your opportunity cost

BOOM. Money is not endless. Time is not endless. You gotta make choices, my Padwan.

Chapter #4: Budgeting

As consultants, we understand budgeting. Many of us have worked in FP&A, or in strategic planning departments. Annual operating plans, monthly operational reviews. S&OP planning processes. We know this stuff. So why is it that 2/5 of Americans don’t follow any type of personal financial budget. It’s a lesson I dearly want the US federal government (and even local governments for that matter) to embrace: please spend less than you make.

.

Great post and tips. The only advice I got when I was young was to put money into a savings account, even then the rate was low! It was only (somewhat) recently, as an adult, that I started to invest. I will be sharing this with all of the “young ones” – thank you!