Recently, I had the opportunity to spend a few hours with 20+ executives to talk about strategy. It was a thought-provoking and courageous conversation. Yes, executives are under enormous pressure to 1) continue to do their day job well (maintain uptime, eliminate risk, ensure customer satisfaction, reduce costs, drive insights, recruit/retain talent, keep everyone happy) while also 2) developing strategies to leapfrog the competition. Who said “work from home” was easy?

If I were summarize the discussion and respond to some of the questions we were not able to address:

Okay, what is strategy?

As a recap, I believe these four icons are a good place to start:

![]()

First, strategy is a set of self-reinforcing activities that gives you a sustainable competitive advantage. It’s not a vision, goal, plan, or culture. It’s what you do to provide unique value to your internal stakeholders (marketing, finance, sales, R&D, manufacturing) or customers that they couldn’t get elsewhere or outsource. It’s the totality of your business model – not just 1 thing – but how it all works together to really differentiate you. Yes, you have smart people. Yes, you have a great IT roadmap and investments. Yes, you have a go-getter culture or responsiveness and collaboration. Yes, it’s all those things – working together – that reinforces itself.

Second, strategy requires trade-offs. It’s impossible to be all things to all people. Peter Drucker – grandfather of management – famously said, “Defending yesterday is far more risky than making tomorrow.” So, yes, we need to meet customer requirements, but also need to be thoughtful on what really delivers value. There are times when we need to manage client’s expectations and help them think through the problem. Just saying yes, can get you in trouble.

A good part of strategy is thinking through: 1) What do we need to be uniquely awesome at? 2) What do we want to be “good enough?”

Third, use best practices as a tool, not a goal:

- Should we learn from the mistakes of others? Of course.

- Should we do the easy, necessary things consistently? Of course.

- Should we be smart and lazy at efficiency-related things? Of course.

Finally, create an economic moat around your business. Know your deep, embedded strengths (read: core competencies). Seek out customers that will love you (read: high willingness-to-pay) and your quality work. Become the default choice (read: higher switching costs), so the customer calls on you to solve their new problems (read: customer lifetime value). Keep the founder’s mentality.

What do you mean by “sustainable competitive advantage”?

Yes, when I first started studying strategy, these are the 3 words that most caught my attention. Sustainable – not just today, or tomorrow, but through multiple business cycles. Think economic moat . . enough to protect your profits long-term. Competitive advantage. Not just matching others or surviving, but thriving.

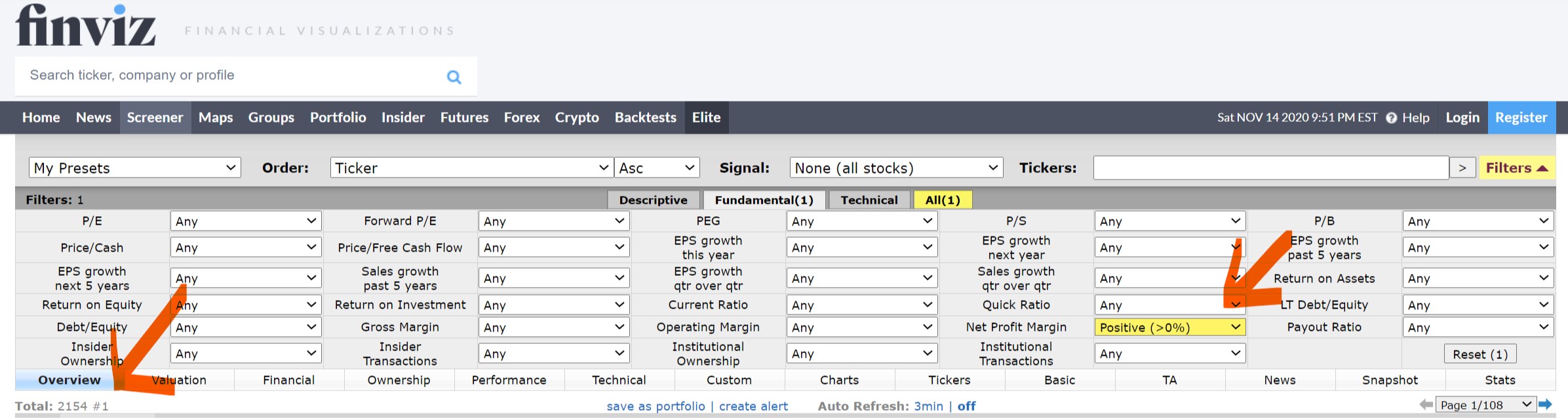

Look, most companies lose money. Yes, this surprised me, but 2/3 of publicly-traded companies in the US (7,600+ when including ADR) lose money here. Put another way, you don’t want to be “average” because being average is bad. This is a screenshot of all companies that have a net margin > 0%. . . 2,154/7,600+

If you are consistently more profitable than you rivals, why is that? It means that you have a good set up – where you are delivering great value to customers who are willing to pay for your services. It’s sustainable because it’s not just a fad, luck, or profits from a waning brand that you inherited. You are in the market, and you are winning at your specific game. Note: average profitability varies dramatically by industry (see finance hero, Aswath Damodaran’s website here).

Want more? Read Competitive Advantage by Michael Porter, 1998, 590+ pages here (affiliate link). I’ve read it. It’s useful and a surprisingly easy read.

Who exactly is the “competition”?

Well, for starters, it’s definitely your everyday rivals. Coke vs. Pepsi. Boeing vs. Airbus. Cisco vs. Huawei. BMW vs. Mercedes. Yes, of course, they are definitely competing for your profits. . . poaching your customers, copying your products, recruiting your (good) employees, and deconstructing your value proposition.

But wait, it’s much worse than that. . . Every time your suppliers raise prices, allocate supply, or reduce service levels, they are chipping away at the value (read: profits) you get to keep. Every time a customer asks you for a discount, or doesn’t renew a contract, they are your competition. Every time a new start-up enters your market and offers a cheaper, disruptive (think: less for less) service, they are your competition. Don’t take this the wrong way, but everyone’s your competition.

Yes, a strategist’s job is to cope with competition.

Isn’t strategic planning the same thing as strategy?

Most people will say no. In the same way that architectural designs are not a house. A recipe is not a pasta dish.

- Agreed, that strategy takes time to do well (see the earlier comparison to digging a medieval castle moat).

- Agreed, a planning process helps to trickle down the strategy to tactical (front-line, day-to-day) implementation.

- Agreed, that cross-functional communication is tough, and therefore, requires a structured annual process.

- Agreed, this all has to eventually filter through FP&A and set budgets.

- Agreed, strategic planning can be bureaucratic. Yes, that’s why strategic planning is not the same thing as strategy.

It’s a useful process, offsite workshop, and document. If you want a spicier answer, read The Big Lie of Strategic Planning, HBR, 2014 (Roger Martin, ex-Dean of Rotman School of Management)

Is strategy the path to an end-point, or the end-point (expected outcome itself)?

Strategy done well is a continuous process for many reasons:

- Strategy takes time and reinvestment; remember, it’s a set of activities not just one thing

- No strategy is evergreen; rivals and new entrants are too smart and hungry to leave you alone

- There’s a lot of craziness out there (think: weather, pandemic, regulation, shifts in technology)

- Customer’s expectations and preference change. (think: AirBnB, StitchFix, Lemonade)

- There is a huge strategy / execution gap; most strategy never sees the light of day

What should we start / stop / continuing doing?

When I read this question, my initial reaction is “It depends“. Does this activity X. . .

- differentiate me from competition, creating customers HIGHER willingness to pay?

- lower my cost structure, giving you higher margins when selling at your competitors’ price?

- fit my resources & capabilities so well that it only makes sense that I should do it?

- make me look great, because I am rocking it. . . doing well (easily)?

- provides me learning and a longer-term economic moat?

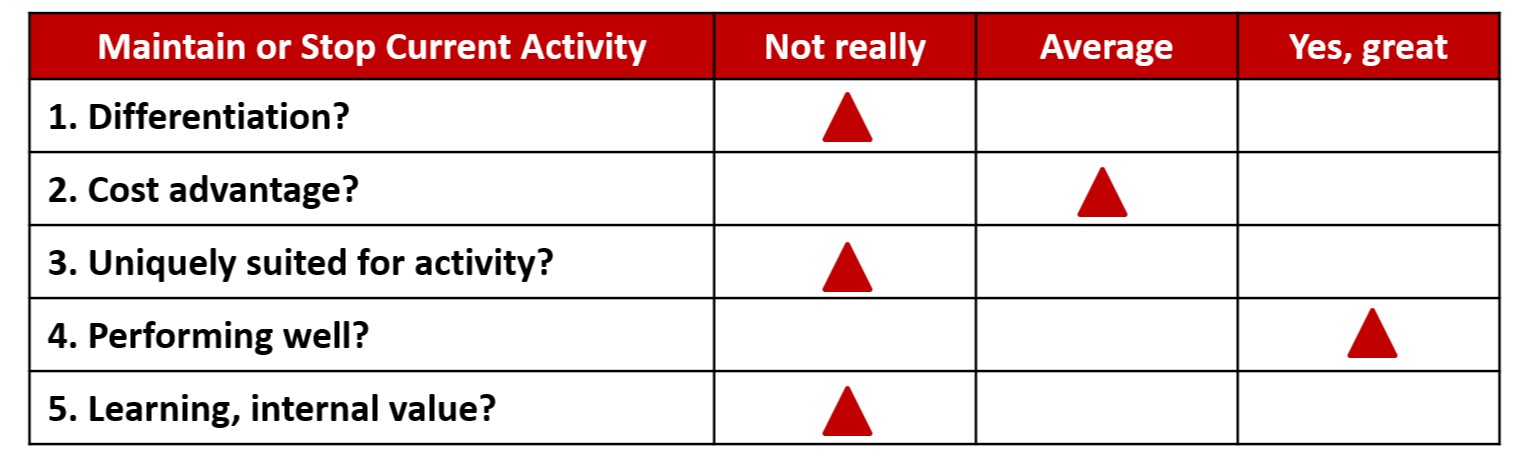

From the hypothetical example below, hmm, given a choice, this is something I would like to outsource or stop. Maybe this change is not possible in the short-term, but think of your work as a portfolio of stocks. Stocks that you buy more of, sell, and hold.

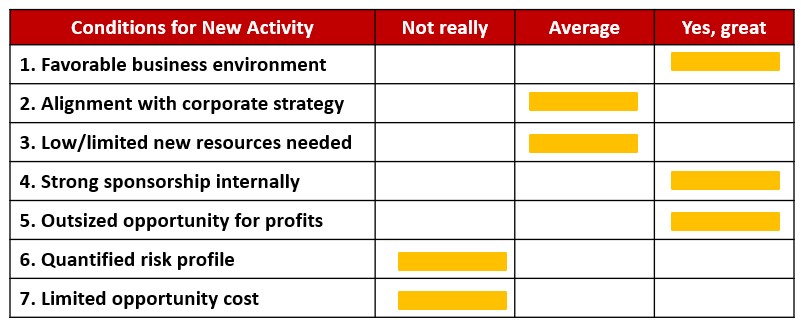

What about a new activity? How might that look different? In my opinion, (yes, this is a n=1 sample size, so definitely get other opinions), I believe this is a decision that depends heavily on the environment (the profitability of the business, your boss, your company etc). Namely, strategy is difficult to do and takes a good bit of time. Do you have the heart, grit, and relational equity to make it happen? Here’s another evaluation matrix:

- How’s the business doing? Profits good? Company have an investment posture?

- Does this line up approximately with the larger corporate strategy?

- What kind of budget and investment are we talking about?

- Do you have the executive VPs on board; are you going to get a round of “heck ya” at a stage/gate meeting?

- Is this something that can help us leapfrog the competition, or a “me too” proposition?

- What’s the risk profile look like? Is it something we’ve assessed? Is it worth it?

- What if we don’t do this, could we better use the money, attention, resources elsewhere?

What are useful ways to underscore strategy for tactical thinkers?

Yes, this is hard. In the day-to-day sprint for results, metrics, meetings and performance reviews – who has the luxury of slow thinking? It’s not easy to think about the long-term strategy, marathon of sustainable competitive advantage. Some things that might help:

- Write it down. What does “winning” look like for your company, department, function, personal career?

- Do you have a board of directors to nudge, motivate, and question you?

- Think backwards from the customer. Who is she? What does she value? How well do you know her?

- Are you making trade offs? What are they? When is the last time you said “no” productively, and used that time for something useful?

- Who else can do this? Are you hoarding work, instead of delegating to juniors who need the opportunity?

- If you could invest 20 hours a week x 5 years to be the best 5% in the world at XYZ. . .what is XYZ?

- Quote from Nike: “Yesterday, you said tomorrow.”

Thank you for the post. I’ve discovered your blog a few months ago and it has become a go-to source of information for me. I would love to get your thoughts on a few things one day if the opportunity presents itself. Kind regards.

Thanks for reading.

keep up the good work and keep writing such beautiful content

Thanks for reading, winning.

Thanks for this post especially emphasizing the need to document trade-offs. I am trying to teach myself the skills of consulting. Do you mind sharing your course syllabus that you teach at Emory? I’d like my summer project to work through a course more systematically. Thank you.

Yes, will send you a link once its up. Thanks.